Siemens SWOT: What 170 Years of Industrial Dominance Actually Looks Like Under the Hood

Siemens' ONE Tech strategy is bold. Its €10.4B net income is real. So is the restructuring of its most profitable division. A 2025 SWOT for strategy professionals who want the full picture.

Introduction

Siemens is one of those companies that's easy to overlook precisely because it's everywhere. Power grids, factory floors, hospital scanners, train systems — if it moves electrons or data at industrial scale, Siemens is probably involved.

But ubiquity isn't the same as invincibility. Fiscal 2025 was, by most measures, a record-breaking year for Siemens. It was also a year the company cut 5,600 jobs. Both things are true, and that tension is exactly what makes this SWOT worth paying attention to.

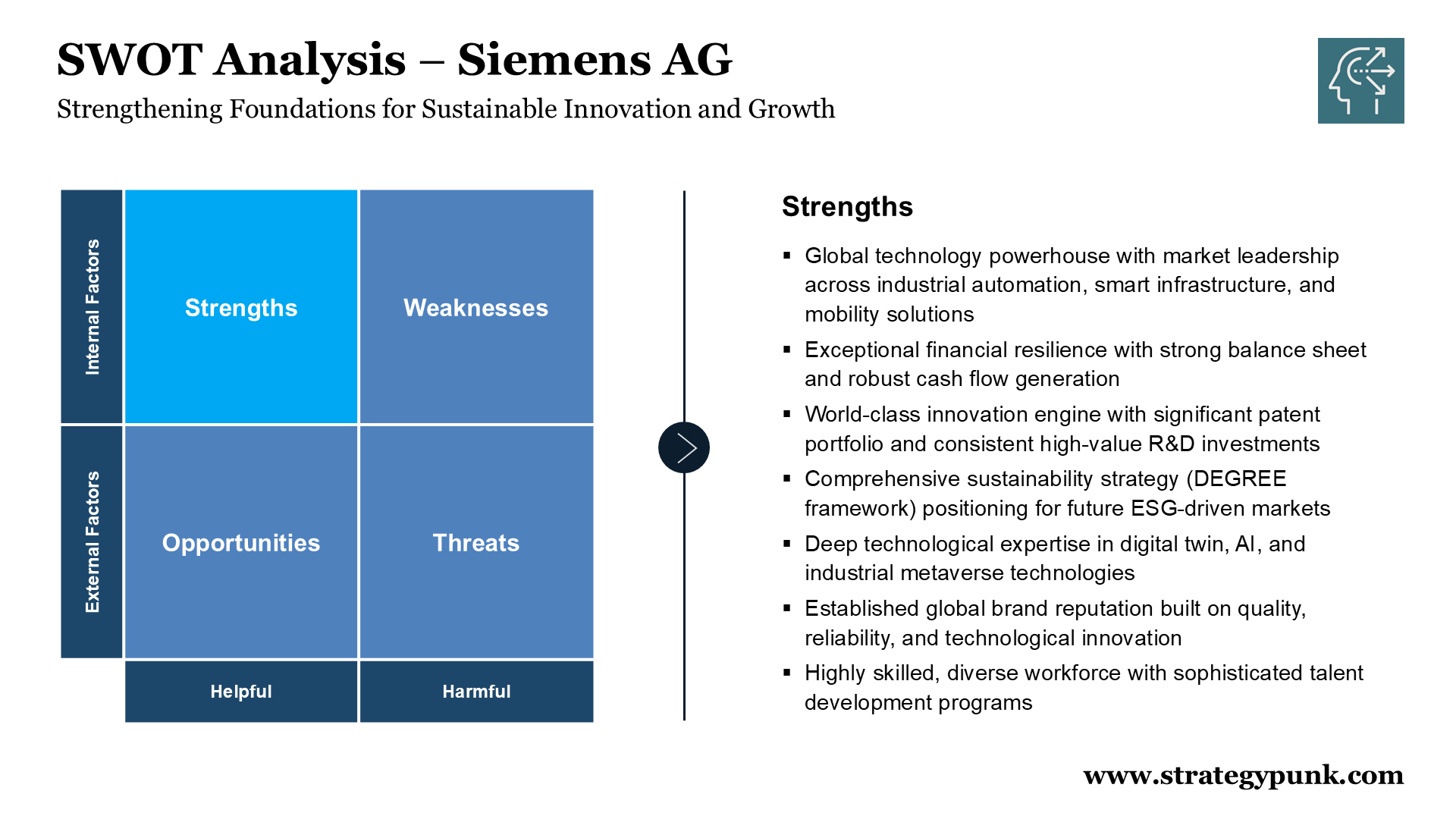

Strengths: A Moat Built Over Decades

The financials are genuinely impressive. Net income rose 16% to €10.4 billion in fiscal 2025, while free cash flow reached an all-time high of €10.8 billion. Euronews Total revenue reached €78.9 billion and orders €88.4 billion. Euronews That's the third consecutive year of record net income — a signal of structural strength, not a lucky quarter.

The ONE Tech strategy is sharpening the focus. Siemens isn't just big — it's becoming more deliberately big. With its ONE Tech Company program, Siemens is raising its mid-term revenue growth ambition to 6–9% and plans to double its digital business revenue, with a €1 billion investment in AI over the next three years. Siemens The acquisitions of Altair Engineering for €9.5 billion and Dotmatics for $5.1 billion aren't defensive moves — they're aggressive bets on industrial simulation, AI, and life sciences software that significantly expand Siemens' addressable market.

The digital bet is paying off. Siemens' total addressable market is growing at approximately 6% annually, reaching €650 billion in five years — with the digital segment within that growing at 11% annually to reach €175 billion by 2030. Siemens The more Siemens embeds its software into a customer's operations, the harder it becomes to switch vendors. That's a moat being built in real time.

Sustainability as a go-to-market strategy. Siemens' DEGREE framework is more than an ESG checklist — it's increasingly a procurement advantage. Governments and corporations under pressure to hit their own climate targets prefer vendors who can help them get there. The company that can electrify a city and prove its carbon credentials simultaneously has a real competitive edge over firms still playing catch-up on ESG.

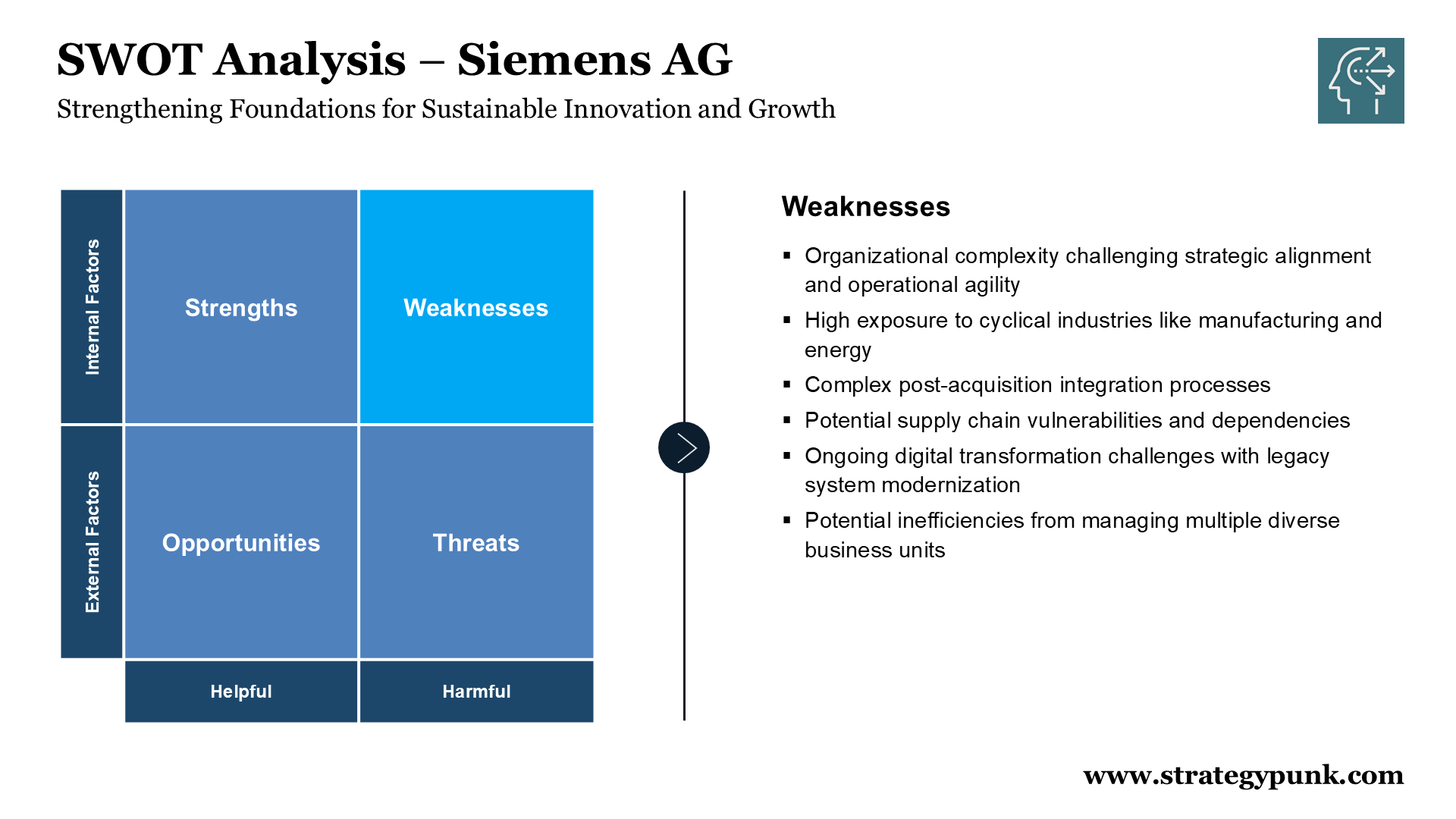

Weaknesses: The Price of Complexity

Digital Industries is the crown jewel that lost its shine. Until recently, Siemens' automation and software division carried the group's highest margins. But muted demand primarily in Germany and China, coupled with increased competitive pressures, considerably reduced orders and revenue in the industrial automation business over the last two years. Yardi Kube The response: cutting 5,600 jobs — the largest reduction at Siemens since 2017 — amounting to about 8% of the segment's 68,000 employees. Yardi Kube When your strongest division requires your biggest restructuring in eight years, that's a structural signal worth taking seriously.

Germany and China exposure is a double vulnerability. Siemens has been struggling amid slowdowns in both China and Europe's biggest economy, which has been mired in recession for two consecutive years. Fortune These aren't peripheral markets — they're core. And the company's customer base in central Europe is further exposed because many of those customers themselves export to China.

Integrating two mega-acquisitions simultaneously is a real operational risk. Absorbing Altair and Dotmatics while restructuring Digital Industries and executing the ONE Tech transformation is a significant organizational load. Coordination costs across a conglomerate of this scale are real, and the risk of strategic misalignment between divisions shouldn't be underestimated.

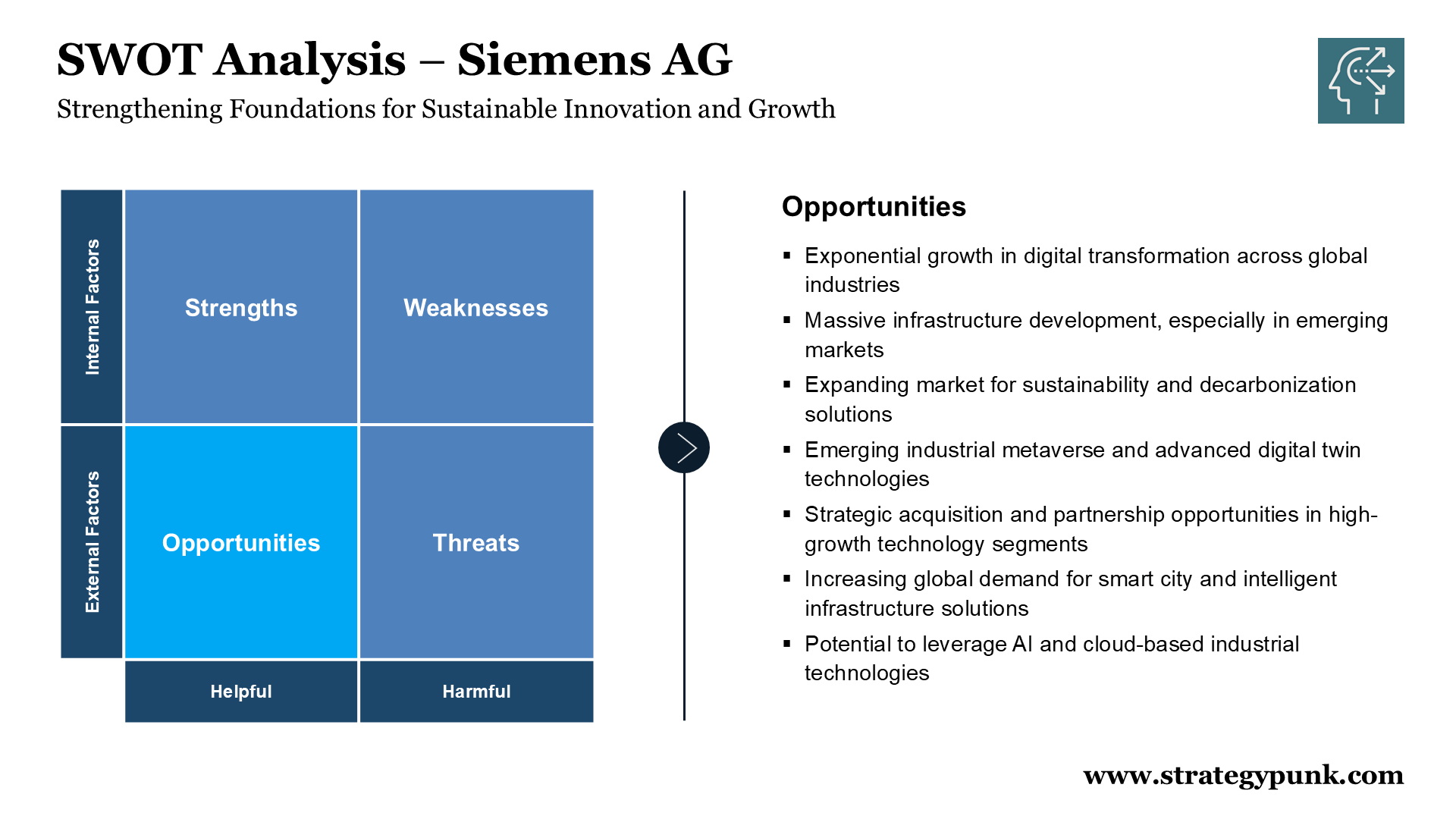

Opportunities: Riding Three Secular Tailwinds

Infrastructure spending is accelerating globally. Governments worldwide — particularly in emerging markets — are investing heavily in modernizing energy grids, transportation networks, and urban systems. Siemens' Smart Infrastructure division is already benefiting: Smart Infrastructure expects comparable revenue growth of 6–9% for fiscal 2025 with a profit margin of 17–18% Siemens — making it one of the group's most reliable performers.

Data centers and electrification are structural growth drivers. AI-driven demand for computing infrastructure is creating a surge in orders for power distribution, switchgear, and grid technology. While orders for electrical products for data centers declined 16% in Q2 due to one large US operator slowing a project Bloomberg, the long-term demand trajectory remains strong. This is a timing issue, not a trend reversal.

The industrial metaverse has a credible business case now. Digital twin technology — creating virtual replicas of physical systems — is moving from concept to standard practice in advanced manufacturing. With Altair's simulation software integrated into the portfolio, Siemens is targeting market expansions worth €50 billion in fiscal 2025, expected to grow at 14–18% annually through 2030. Siemens That's not a moonshot. That's a roadmap.

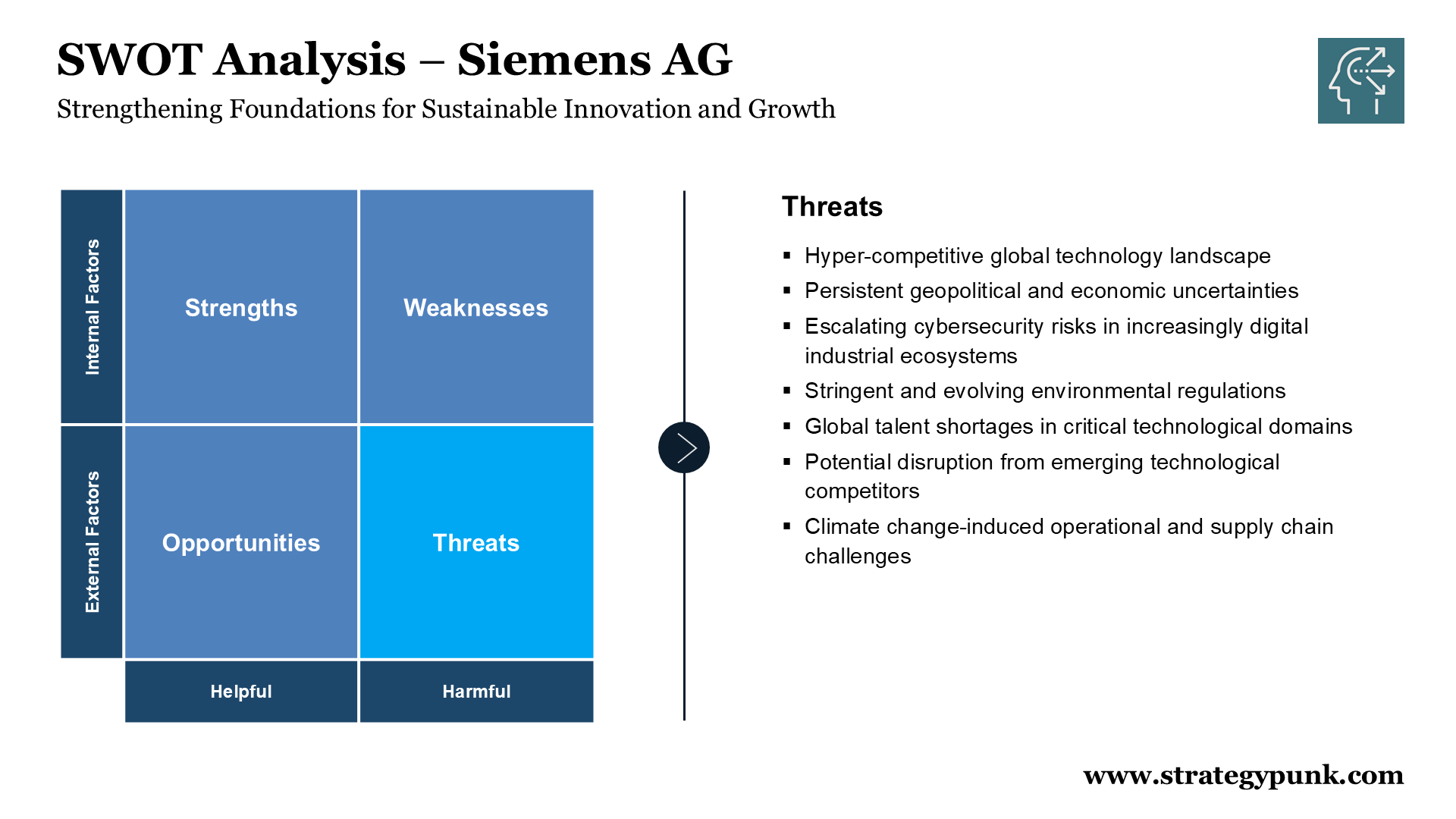

Threats: The Risks That Keep Executives Up at Night

Geopolitics is the wildcard nobody can model. Siemens warned that "substantial burdens from currency effects" would weigh on reported growth and profitability in fiscal 2026. Euronews Beyond FX, the company operates in virtually every major economy — which means trade restrictions, regional conflict, and policy uncertainty create fragility that doesn't show up cleanly on a balance sheet. The EU's evolving AI Act regulations, which Siemens has lobbied policymakers to clarify, add another layer of policy risk.

Cybersecurity is an existential operational concern. As industrial infrastructure becomes a target for sophisticated cyberattacks — nation-state level included — a company sitting at the intersection of energy, transport, manufacturing, and now life sciences software is a high-value target by definition. This isn't a line item. It's a strategic priority that requires continuous investment with no clear finish line.

The talent problem is quietly the most dangerous long-term threat. The global shortage of engineering and AI talent may be the constraint that most limits Siemens' growth over the next decade. Siemens can outspend most competitors on R&D — it's committing €1 billion to AI alone over the next three years Siemens — but if it can't hire the people to execute at pace, the strategy stalls. Restructuring 5,600 jobs out of Digital Industries while simultaneously needing to attract AI and software talent in a competitive market is a delicate balancing act.

Fiscal 2025 confirmed something important: Siemens' core thesis — combining the real and digital worlds — is structurally sound.

The records in net income and free cash flow prove the model works. But the simultaneous restructuring of its most prestigious division reveals that even the strongest industrial conglomerates aren't immune to cyclical gravity.

The question worth sitting with: as Siemens accelerates its shift toward software and AI, can a 170-year-old industrial giant genuinely out-compete software-native players on their own turf — or will it always be one economic slowdown away from cutting the very engineers it needs most?