Novo Nordisk SWOT Analysis: Navigating the GLP-1 Arms Race

Novo Nordisk created the GLP-1 category, but Lilly is closing fast. A strategic breakdown of the oral Wegovy bet and what it means for market share. Download the full SWOT analysis PDF.

Introduction

The pharmaceutical landscape is currently defined by one dominant narrative: the explosion of the GLP-1 receptor agonist market. At the center of this medical and financial revolution stands Novo Nordisk.

The Danish pharmaceutical giant essentially created the GLP-1 category and continues to lead it. The terrain is shifting rapidly. With competitors closing the gap in efficacy and new formats entering the market, Novo Nordisk faces a critical juncture. The launch of oral Wegovy represents perhaps the most significant commercial event the company has executed in a decade.

This SWOT analysis examines Novo Nordisk’s current strategic position, highlighting the strengths that built their empire, the weaknesses they must address, the opportunities ahead, and the threats on the horizon.

Strengths: The Foundation of a Market Leader

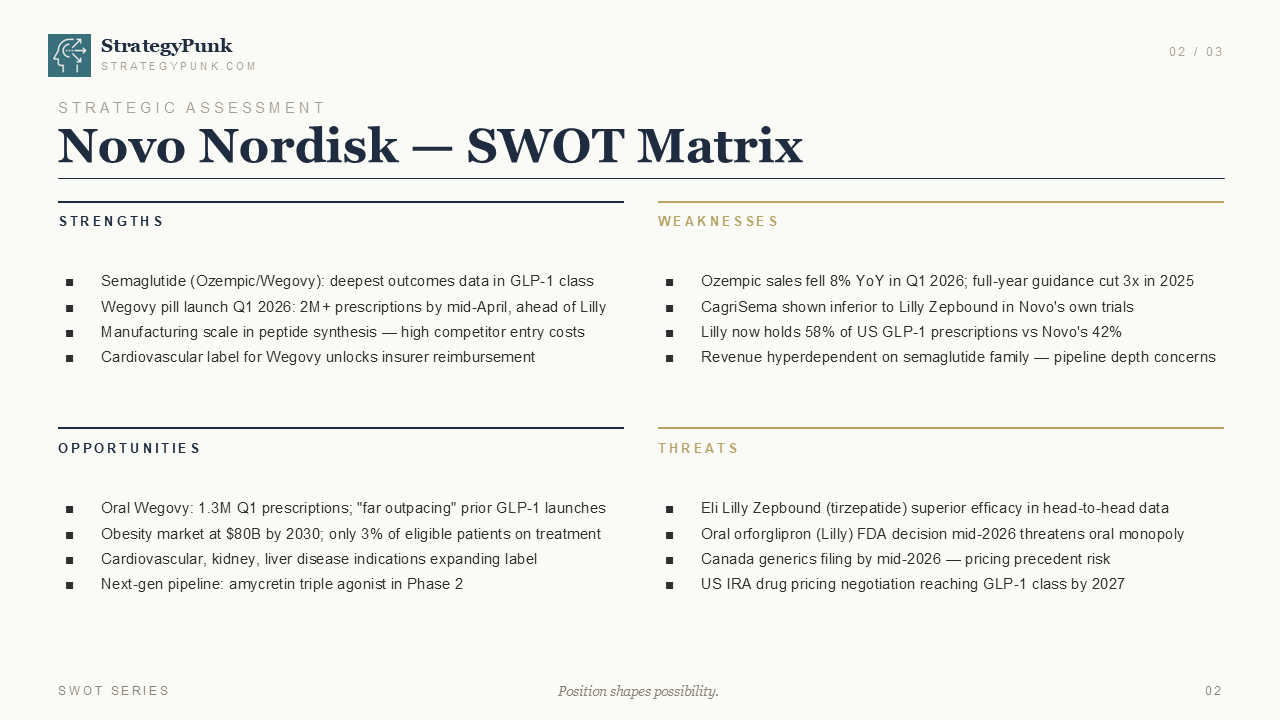

Novo Nordisk’s position is not accidental; it is built on a foundation of deep clinical data, massive manufacturing scale, and strategic label expansion. The company's semaglutide franchise, which includes both Ozempic and Wegovy, possesses the deepest outcomes data in the entire GLP-1 class. This extensive clinical history provides a significant advantage in reassuring both prescribers and patients about long-term safety and efficacy profiles.

A critical recent victory for Novo Nordisk is securing a cardiovascular label for Wegovy. This is a game-changer. By demonstrating that Wegovy reduces the risk of major adverse cardiovascular events, Novo Nordisk has effectively unlocked broader reimbursement from insurers. It transforms the drug from a weight-loss treatment into a critical cardiovascular intervention, shifting the economic conversation with payers. The label expansion is a strategic masterstroke that significantly broadens the drug's appeal and necessity.

The launch of the Wegovy pill in Q1 2026 has been a resounding success. Securing over two million prescriptions by mid-April, Novo Nordisk has established a strong foothold ahead of key competitors like Eli Lilly in the oral medication space. This rapid uptake demonstrates the massive latent demand for a non-injectable option and validates Novo Nordisk's strategy to capture this segment early.

Underpinning all of this is Novo Nordisk's massive manufacturing scale in peptide synthesis. The infrastructure required to produce these complex molecules at scale is immense. This established capacity creates a strong barrier to entry for new competitors in the GLP-1 market. Building this capacity takes years and billions of dollars, providing Novo Nordisk with a structural advantage that is difficult to replicate quickly.

Weaknesses: Vulnerabilities in the Armor

Despite their dominant position, cracks are visible in Novo Nordisk's armor. The most pressing issue is the shifting competitive dynamic, particularly against their primary rival, Eli Lilly. The data is clear: Lilly is winning the efficacy battle. In Novo Nordisk's own trials, its combination therapy, CagriSema, was shown to be inferior to Lilly’s Zepbound. This efficacy gap is translating directly into market share. Lilly now commands 58% of US GLP-1 prescriptions, leaving Novo Nordisk with 42%. The first-mover advantage is meeting second-mover efficacy, and efficacy is currently winning the prescription pad.

Financial indicators also show areas of concern. Ozempic sales declined 8% year over year in Q1 2026. This softening led the company to cut its full-year guidance three times in 2025, signaling volatility and perhaps a faster-than-expected erosion of its dominant market position. This trend suggests that while the overall market is growing, Novo Nordisk's slice of the pie might be under more pressure than initially anticipated.

Zooming out, Novo Nordisk faces a structural weakness: hyperdependence on revenue from the semaglutide family. Their financial health is inextricably linked to this single molecule. This lack of diversification raises serious concerns about pipeline depth. If semaglutide faces unforeseen regulatory hurdles, severe pricing pressure, or is definitively outclassed by next-generation competitors, Novo Nordisk has limited alternative revenue engines to fall back on. This concentration risk is a significant vulnerability in a fast-moving therapeutic area.

Opportunities: Expanding the Pie

The opportunities available to Novo Nordisk are as massive as the market itself. The sheer scale of the addressable market is staggering. The global obesity market is projected to reach $80 billion by 2030. Currently, only 3% of eligible patients are receiving treatment. The ceiling for growth is exceptionally high, providing a vast runway for both Novo Nordisk and its competitors.

The primary vehicle for capturing this growth is Oral Wegovy. The early numbers are highly promising, with 1.3 million prescriptions in Q1 alone, a pace that is "far outpacing" prior GLP-1 launches. This indicates a strong market appetite for the oral format and suggests that the pill could be the key to unlocking the remaining 97% of the untreated market.

Oral Wegovy represents Novo Nordisk's key strategic bet. It serves as the mass-market entry point. The strategy is to convert the 97% of eligible patients who are currently priced out of, or hesitant about, injectable GLP-1s into a massive, recurring revenue base. The pill is the pivot. By lowering the barrier to entry—both in terms of cost and patient preference—Novo Nordisk aims to establish a new standard of care in obesity management.

Beyond obesity and diabetes, the opportunity lies in expanding the label for semaglutide. Research into cardiovascular, kidney, and liver disease indications could open entirely new patient populations and reimbursement channels, further solidifying the drug's essential status. If semaglutide can prove efficacy across a broader spectrum of metabolic diseases, its value proposition increases exponentially.

Looking to the future, Novo Nordisk must deliver on its next-generation pipeline. The amycretin triple agonist, currently in Phase 2 trials, represents their potential answer to the escalating efficacy war. Success here is critical to maintaining long-term market leadership. If amycretin can match or exceed the efficacy of tirzepatide, Novo Nordisk will be well-positioned to defend its market share.

Threats: The Gathering Storm

The threats facing Novo Nordisk are substantial and immediate, stemming from both aggressive competition and shifting regulatory environments. The most acute threat is Eli Lilly's Zepbound (tirzepatide). Its demonstrated superior efficacy in head-to-head data is a fundamental challenge to Novo Nordisk's market share. Patients and physicians will naturally gravitate toward the most effective treatment, putting immense pressure on semaglutide.

The oral market, currently a bright spot for Novo, is also under threat. An FDA decision on Lilly's oral orforglipron is expected in mid-2026. If approved, this will immediately threaten Novo Nordisk's oral monopoly, likely triggering a price war and aggressive marketing battles. The entry of a direct competitor in the oral space will test the resilience of Novo Nordisk's early lead.

Pricing pressures are mounting globally. In Canada, generic filings are expected by mid-2026. This introduces a significant risk of pricing precedent. If cheaper alternatives enter the Canadian market, it will exert downward pressure on prices globally. The globalization of pharmaceutical pricing means that a crack in one market can quickly spread to others.

In the United States, the regulatory environment is tightening. The Inflation Reduction Act (IRA) drug pricing negotiations are projected to reach the GLP-1 class by 2027. This government intervention could severely compress margins in Novo Nordisk's most lucrative market. The potential for mandated price cuts represents a significant headwind for future profitability.

The Strategic Bet: What to Watch

Novo Nordisk created the GLP-1 category, but the landscape has changed. The launch of oral Wegovy is their defining move for the current era. We believe accessibility and convenience can offset the superior efficacy of injectable competitors. As this strategy unfolds, industry observers should monitor three critical metrics:

- Oral vs. Injectable Mix: The key question is whether the pill format cannibalizes existing Wegovy injections or if it successfully expands the overall market pie by bringing in new patients. A high rate of cannibalization would be concerning, while significant market expansion would validate the strategy.

- Lilly's orforglipron: The timing of its FDA approval and its pricing strategy relative to the oral Wegovy launch will dictate the competitive dynamics of the oral market. A swift approval and aggressive pricing strategy from Lilly could blunt Novo Nordisk's momentum.

- Pipeline Credibility: All eyes are on the Phase 2 data for Amycretin. Novo Nordisk must prove it has a next-generation answer to tirzepatide to reassure investors of its long-term viability. Positive data here is essential for maintaining confidence in the company's prospects.

Novo Nordisk remains a titan in the pharmaceutical industry, but they are operating in an increasingly hostile environment. The GLP-1 arms race is far from over, and the next few years will determine whether the pioneer can maintain its crown against a formidable challenger. The strategic decisions made today will echo for decades in the metabolic disease space.

Download the Novo Nordisk SWOT Analysis

Want to dive deeper into the strategic position of Novo Nordisk?

Download the complete SWOT analysis PDF below for a concise, visual breakdown of the company's current standing in the GLP-1 market.