From Auto Parts to Europe’s Arms Dealer: The Rheinmetall SWOT Analysis

Europe is rearming — and Rheinmetall is holding the blueprints. A sharp SWOT breakdown of the company turning a €135B backlog into a decade of compound growth.

Introduction

Europe is building the army it should have built a decade ago. And right at the center of this massive, continent-wide rearmament sits one company: Rheinmetall.

Once known primarily as an auto-parts supplier with a defense division, the Düsseldorf-based giant has undergone a radical transformation. Today, it stands as Europe's premier full-spectrum defense integrator. But with rapid growth comes immense pressure. Can they deliver on a backlog that looks more like a small country's GDP?

Let's dive into the strategic reality of Rheinmetall, breaking down their strengths, weaknesses, opportunities, and threats to understand what’s really driving this defense powerhouse.

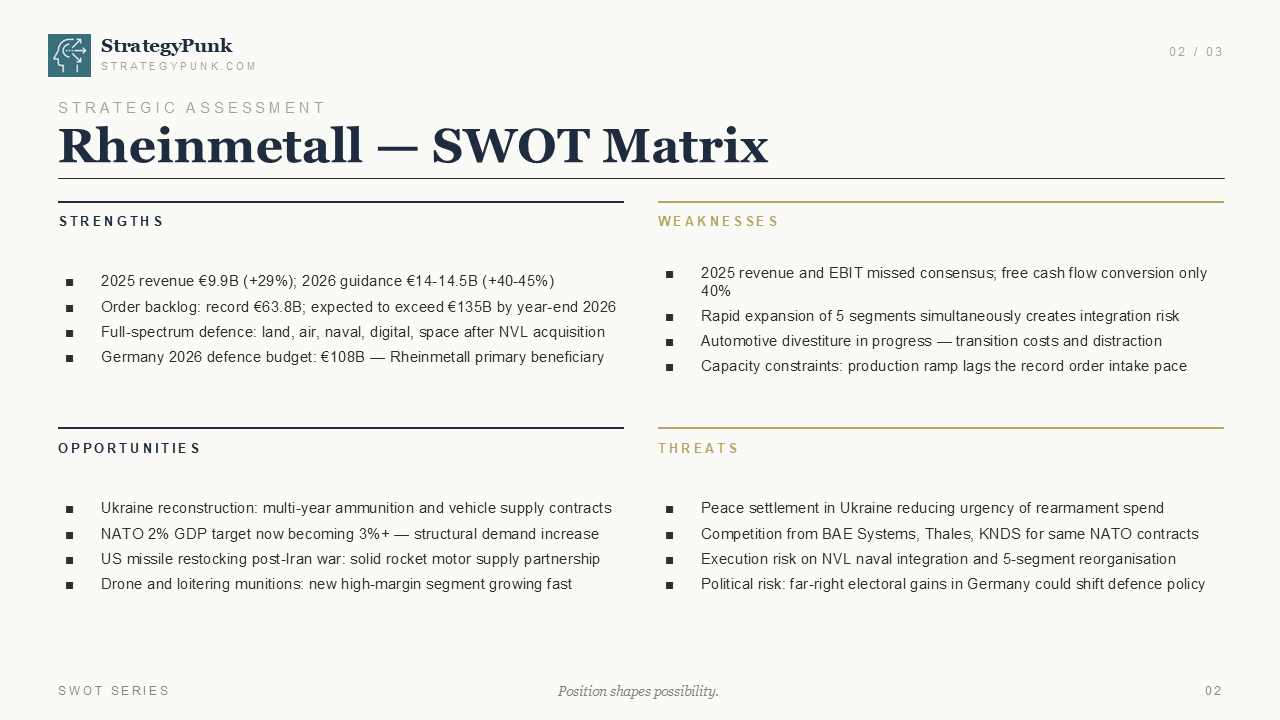

Strengths: The Unprecedented Backlog

Rheinmetall is sitting on a mountain of orders. The numbers are staggering: a record €63.8 billion order backlog, which is expected to blow past €135 billion by the end of 2026.

This isn't just a bump in demand; it's a structural shift. With Germany committing to a €108 billion defense budget in 2026, Rheinmetall is positioned as the primary beneficiary. They have evolved into a full-spectrum defense provider covering land, air, naval, digital, and space domains, especially after their strategic NVL acquisition.

"Rheinmetall has transformed from an auto-parts supplier with a defence division into Europe's premier full-spectrum defence integrator."

This full-spectrum capability means they aren't just selling parts; they are selling integrated warfare systems. When governments write massive checks, they want a single-source prime contractor. Rheinmetall has positioned itself to be exactly that.

Weaknesses: The Pains of Hypergrowth

Growth is great, but hypergrowth breaks things. Rheinmetall is experiencing the classic growing pains of a company trying to scale too fast.

First, their 2025 revenue and EBIT missed consensus, and their free cash flow conversion sits at a concerning 40%. They are bringing in cash, but the costs of scaling are eating into it.

Second, they are expanding five segments simultaneously. This creates massive integration risk. Adding to the complexity is the ongoing divestiture of their automotive division. This transition brings costs and, more dangerously, strategic distraction.

Finally, capacity constraints are real. The production ramp simply lags behind the record order intake pace. It's one thing to win a €135 billion backlog; it's another entirely to build and deliver those systems on time.

Opportunities: The Structural Demand Shift

The geopolitical landscape has permanently altered the defense market. The NATO 2% GDP defense spending target is rapidly becoming a 3%+ reality. This isn't a temporary spike; it's a long-term, structural demand increase.

Beyond the immediate European rearmament, Ukraine's reconstruction presents multi-year ammunition and vehicle supply contracts. Rheinmetall is perfectly positioned to capture this long-tail revenue.

There are also new, high-margin frontiers. The drone and loitering munitions segment is growing fast, offering better margins than traditional heavy armor. Additionally, the US needs to restock missiles post-Iran conflict, and Rheinmetall's solid rocket motor supply partnership opens the door to the lucrative American market.

Threats: The Execution Reality

Position shapes possibility, but execution determines survival. The biggest threat to Rheinmetall isn't a lack of demand; it's the risk of fumbling the execution.

The integration of the NVL naval acquisition and the broader 5-segment reorganization carries massive execution risk. If they stumble, competitors like BAE Systems, Thales, and KNDS are waiting to poach those lucrative NATO contracts.

Then there is the political reality. A peace settlement in Ukraine could rapidly reduce the urgency of rearmament spending. Furthermore, political shifts within Germany, specifically far-right electoral gains, could alter defense policy and spending priorities.

The Strategic Bet: No Going Back

Rheinmetall is making a massive strategic bet: become Europe's single-source defense prime. They want the backlog and margin profile to fund a decade of compound growth.

But to pull this off, they have to navigate the transition flawlessly. There are three critical things to monitor moving forward:

- FCF Conversion: Will that 40% free cash flow conversion improve as integration costs normalize?

- Ukraine Resolution: How will a potential peace settlement impact near-term ammunition and vehicle demand?

- NVL Naval Integration: Can they execute the shipbuilding acquisition and actually realize the margin contribution?

The backlog is real. The execution risk is real too. From auto parts to artillery, with €135 billion in orders on the line, there is no going back.

Will Rheinmetall successfully digest its massive backlog, or will the friction of hypergrowth slow them down?

Download the full Rheinmetall SWOT Analysis PDF here:

Stay ahead of the curve. Sign up for the StrategyPunk newsletter for more deep dives into the strategies shaping our world.