Palantir SWOT Analysis: The AI Platform Governments and Enterprises Trust (Free PDF)

Discover our Palantir SWOT Analysis: exploring AIP's growth, ontology moats, and the massive risks in enterprise AI. Free PDF Analysis download.

Introduction

Palantir spent two decades building the infrastructure for a moment that arrived in 2023. AIP is the product. The Ontology is the moat. The question is whether the valuation assumes a future that arrives on schedule.

Let's break down the strategic landscape for Palantir. They are positioning themselves as the enterprise AI operating system. Think of it as the governance and deployment layer for agentic AI across government and commercial clients globally. This isn't just about throwing an LLM at a problem; it's about embedding AI into the operational fabric of massive organizations.

Strengths: The Foundation of Trust

Palantir's core strengths are rooted in robust product offerings and deep integration into critical government and commercial operations. They aren't just selling software; they are selling a fundamental shift in how organizations process reality.

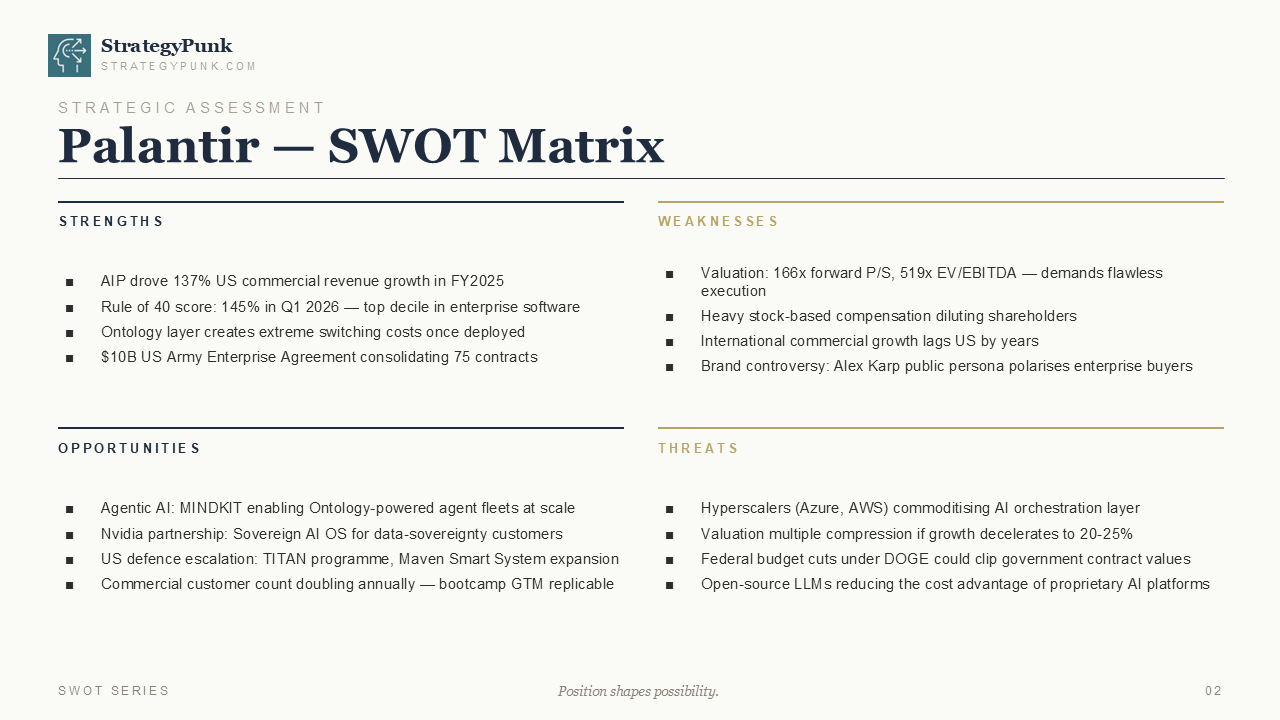

AIP Driving Commercial Growth: The Artificial Intelligence Platform (AIP) is a massive growth engine. In FY2025, AIP drove staggering 137% growth in US commercial revenue. This isn't a pilot program. It's a fundamental shift in how enterprises adopt Palantir's technology. They are moving beyond the defense sector and proving their value in the commercial space at an unprecedented rate.

Financial Performance: Palantir boasts a Rule of 40 score of 145% in Q1 2026. This places them squarely in the top decile of enterprise software companies. It demonstrates an exceptional balance of growth and profitability. You rarely see this level of hyper-growth combined with such strong unit economics.

The Ontology Moat: The Ontology layer creates extreme switching costs once deployed. When a company integrates its data and operations into Palantir's ontology, ripping it out becomes a monumental, high-risk task. This stickiness is a massive competitive advantage. It's not just a database; it's a semantic representation of the entire enterprise.

Government Consolidation: The $10B US Army Enterprise Agreement, consolidating 75 contracts, highlights Palantir's entrenched position in the defense sector. They aren't just a vendor. They are the infrastructure. This level of lock-in provides a stable, highly lucrative revenue base that is incredibly difficult for competitors to disrupt.

Weaknesses: The Valuation Question

While Palantir has strengths, it faces significant challenges that require flawless execution. The market has priced them for perfection, and any misstep will be heavily penalized.

Valuation Demands Perfection: Trading at 166x forward P/S and 519x EV/EBITDA, the market has priced in years of perfect execution. Any misstep or slowdown in growth will likely trigger a harsh market reaction. The margin of safety here is practically non-existent. They must deliver on the hype.

Shareholder Dilution: Heavy stock-based compensation continues to dilute shareholders. While necessary for attracting top talent in a hyper-competitive AI market, it remains a drag on earnings per share. Investors are tolerating this for now due to the growth, but patience isn't infinite.

International Lag: International commercial growth lags the US by years. The AIP bootcamp model, so successful domestically, needs to prove it can scale effectively across Europe and Asia-Pacific. The cultural and regulatory landscapes are different, and the US playbook might not translate perfectly.

Brand Controversy: Alex Karp's public persona polarizes enterprise buyers. While his outspoken nature resonates with some and builds a cult-like following, it can alienate others. This potentially complicates the sales process in more conservative corporate environments where risk aversion is the norm.

Opportunities: The Agentic Future

The future offers massive avenues for expansion, provided Palantir can execute on its vision. They are positioned to capture the next major wave of enterprise value creation.

Agentic AI at Scale: The introduction of MINDKIT, enabling Ontology-powered agent fleets at scale, positions Palantir at the forefront of the next wave of AI adoption. This moves beyond chat interfaces to autonomous agents executing complex workflows. This is where the real ROI of AI will be realized, and Palantir is building the infrastructure to support it.

Sovereign AI OS: The Nvidia partnership creates a Sovereign AI OS for data-sovereignty customers. This offering is critical for nations and highly regulated industries that need absolute control over their AI infrastructure and data. As geopolitical tensions rise, data sovereignty will become a massive tailwind.

Defense Escalation: Programs like TITAN and the Maven Smart System expansion signal rising US defense spending. Palantir is perfectly positioned to capture this trend. They have the clearances, track record, and technology to lead the next generation of defense procurement.

Commercial Expansion: The number of commercial customers is doubling annually. The bootcamp Go-To-Market (GTM) strategy is proving highly replicable, accelerating enterprise adoption. This land-and-expand model is working, and the runway for commercial growth is massive.

Threats: The Hyperscaler Challenge

The competitive landscape is fierce, and Palantir must navigate significant external risks. They are playing in a market dominated by tech giants with deep pockets and massive distribution advantages.

Commoditization of the Orchestration Layer: Hyperscalers like Azure and AWS are aggressively commoditizing the AI orchestration layer. Azure Foundry and AWS Bedrock are replicating AIP's ontology-based features. This threatens Palantir's unique value proposition. The hyperscalers want to own the entire stack, and they view Palantir as a threat to that ambition.

Valuation Compression Risk: If growth decelerates to the 20-25% range, Palantir faces severe compression of its valuation multiple. The current stock price assumes hyper-growth. Anything less is a massive risk. The market is unforgiving of growth stocks that stumble.

Federal Budget Uncertainty: Potential federal budget cuts under initiatives such as DOGE could reduce government contract values. This would impact a significant portion of Palantir's revenue. While their defense position is strong, they are not immune to macro-level budget pressures.

Open-Source Alternatives: The rapid advancement of open-source LLMs reduces the cost advantage of proprietary AI platforms. This could potentially pressure margins and pricing power. As open-source models become "good enough" for many enterprise use cases, the willingness to pay premium prices for proprietary solutions may wane.

The Strategic Bet

Commodity cognition. Scarce deployment. That is the Palantir bet.

Palantir is betting that while AI models (cognition) will become commoditized, the ability to securely and effectively deploy them across complex enterprise environments (deployment) will remain scarce. The ontology is the moat. The valuation is the risk.

They are essentially saying that having the smartest LLM doesn't matter if you can't integrate it into your operational reality. Palantir provides that integration layer.

Three Things to Monitor:

- Multiple Sustainability: Can 30-40% revenue growth in 2026 justify a 100x+ sales multiple? The math gets very difficult if growth slows even slightly.

- International Commercial: Can the AIP bootcamp model scale outside the US into the EU and Asia-Pacific? This is critical for sustaining long-term growth.

- Hyperscaler Response: How effectively will Azure and AWS replicate AIP's core features? The battle for the enterprise AI operating system will be fought against the hyperscalers.

The Bottom Line

Palantir is a fascinating company operating at the bleeding edge of enterprise software. They have built an incredibly powerful platform with a deep moat. The valuation, however, requires a strong stomach and a belief that they can execute flawlessly for years to come. The transition from a defense contractor to a ubiquitous enterprise AI platform is underway, but the journey is far from over.

Download the Full Analysis

Want to dive deeper into the numbers and strategic implications? We've compiled a comprehensive SWOT analysis PDF that breaks down Palantir's position in granular detail.

Download the Palantir SWOT Analysis PDF

Stay Ahead of the Curve

The AI landscape is shifting rapidly. Don't miss out on our latest strategic teardowns and industry insights. Sign up for the StrategyPunk newsletter today and get actionable intelligence delivered straight to your inbox.