Saudi Aramco SWOT Analysis: 5 Strategic Truths About The Last Barrel Standing

The energy transition is real, but Saudi Aramco is positioned to be the last barrel standing. This SWOT analysis breaks down the 5 counter-intuitive strategic truths shaping the world's most profitable oil company.

The energy transition is real. But it is slow. And when the dust settles, Saudi Aramco will likely be the last barrel standing.

For years, the conversation around the energy sector has been dominated by the rapid acceleration of electric vehicles and the pivot toward renewables. We've heard endless predictions about peak oil demand, stranded assets, and the inevitable decline of Big Oil. Yet, looking closely at Saudi Aramco's strategic positioning reveals a much more nuanced — and formidable — reality. They aren't just surviving the transition; they are actively positioning themselves to win the endgame.

Drawing from the latest StrategyPunk SWOT analysis, here are the five most critical, surprising, and impactful takeaways about Saudi Aramco's strategic bet. These aren't obvious points. Some of them will genuinely challenge how you think about the future of energy.

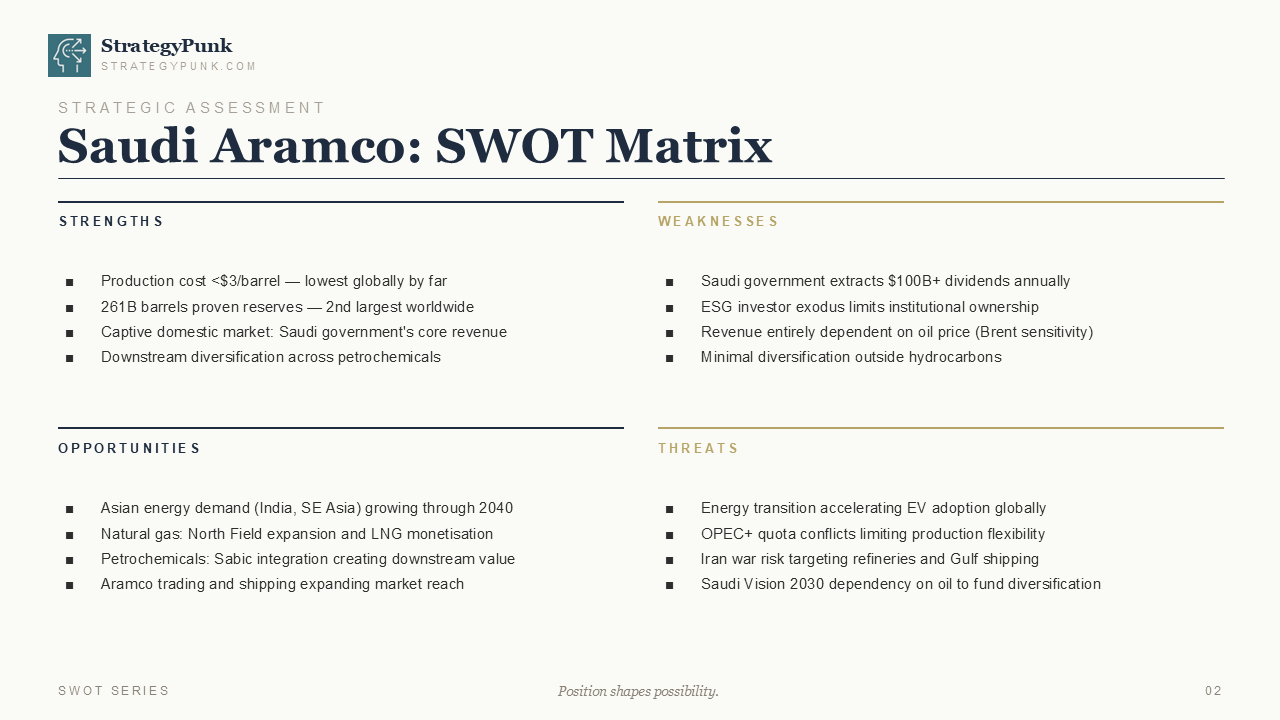

1. The Sub-$3 Barrel Is Not Just a Cost Advantage — It's a Structural Moat

Saudi Aramco produces oil at less than $3 per barrel. Let that sink in for a moment.

This isn't just a cost advantage; it's a structural moat that is nearly impossible for competitors to breach. While North American shale producers and offshore deepwater projects grapple with break-even prices in the $40 to $60 range, Aramco operates in a completely different financial universe. Even at $20 oil — a price that would devastate virtually every other major producer — Aramco remains profitable.

This hyper-low production cost means Aramco survives severe price collapses that force competitors into bankruptcy or asset sales. As the energy transition progresses and global demand eventually tapers, higher-cost producers will be forced out of the market first. Aramco's strategy is simple but devastatingly effective: remain the marginal-cost winner. By maintaining the lowest-cost basis globally, they ensure that their 261 billion barrels of proven reserves — the second-largest worldwide — will be the last to become economically unviable.

"Aramco is the lowest-cost producer in the most capital-intensive commodity on earth. The energy transition is real. But it is slow. And Aramco will be the last barrel standing."

This fundamental truth shapes their entire strategic posture. They don't need to panic about the transition; they just need to outlast the competition. In a market where the question is no longer if demand will decline but how fast, being the lowest-cost producer is the single most durable competitive advantage in the industry.

2. The $100 Billion Dividend Dilemma: Strength and Vulnerability in One Number

Aramco's greatest strength is inextricably linked to its most significant vulnerability: the Saudi government.

The Saudi state extracts over $100 billion in dividends annually from Aramco. This captive domestic market dynamic means the government's core revenue is almost entirely dependent on the company's performance. Aramco is the engine funding Saudi Vision 2030, the ambitious national plan to diversify the economy away from oil dependence.

This creates a fascinating paradox. Aramco must pump vast amounts of cash upward to fund the country's diversification, yet this massive dividend burden restricts the company's own capital flexibility. The money that could be reinvested in new projects, technology, or downstream expansion is instead flowing directly into state coffers. And because revenue is entirely dependent on Brent crude pricing, any sustained oil price collapse doesn't just hurt Aramco's balance sheet — it threatens the entire Saudi economic transformation plan.

The irony is stark. The company that is supposed to fund Saudi Arabia's post-oil future is itself trapped in a near-total dependency on oil revenues. If the transition accelerates faster than expected, the fiscal pressure on the Saudi government could become acute, forcing difficult choices between maintaining dividends and investing in Aramco's own long-term competitiveness.

3. The Pivot to Petrochemicals and Asia Is the Real Growth Strategy

Aramco isn't simply waiting for the end of oil. They are actively reshaping what kind of oil company they want to be.

The integration with SABIC (Saudi Basic Industries Corporation) represents a massive strategic pivot to create downstream value beyond combustible fuels. As EV adoption accelerates and transport fuel demand eventually peaks, the demand for plastics, synthetics, fertilizers, and advanced materials will persist — and in many categories, continue to grow. By dominating the petrochemical supply chain, Aramco hedges against the decline in traditional transport fuels while capturing value from the same hydrocarbon molecule further down the value chain.

Simultaneously, Aramco is locking in long-term supply contracts across Asia, particularly in India and Southeast Asia, where energy demand is projected to grow steadily through 2040. These are markets where energy access, economic development, and industrial growth are still in full swing. The West may be accelerating its energy transition, but billions of people in the developing world are still building the infrastructure that runs on oil and gas. Aramco is positioning itself as the preferred supplier for that growth.

The expansion of Aramco's trading and shipping capabilities further reinforces this strategy. This isn't a company in retreat. It's a company methodically securing its position in the markets that will matter most over the next two decades.

4. The Geopolitical Tightrope: Iran, OPEC+, and the Strait of Hormuz

No analysis of Aramco is complete without confronting the severe geopolitical threats that sit directly on top of its operations.

The primary near-term risk is not the energy transition — it's regional instability. The threat of conflict with Iran, specifically targeting Saudi refineries and shipping routes through the Strait of Hormuz, remains a critical and underappreciated vulnerability. A significant disruption in this chokepoint — through which roughly 20% of the world's oil supply passes — could send immediate shockwaves through global energy markets and severely impact Aramco's ability to deliver its product to customers.

There is also the internal OPEC+ dynamic to consider. Quota conflicts between member states limit Aramco's production flexibility. When Aramco needs to ramp up output to capture market share or respond to a price spike, it is constrained by a cartel agreement that must balance the interests of over a dozen countries with divergent fiscal needs. This is a structural limitation on Aramco's ability to fully monetize its cost advantage.

These geopolitical realities force Aramco to maintain a defensive posture, investing heavily in security infrastructure and redundant logistics. They control the cost of production, but they cannot fully control the security of their export routes. Any serious investor or strategist must weigh this persistent war risk carefully against the company's undeniable financial strengths.

5. The ESG Exodus Is Quietly Reshaping Aramco's Capital Access

Aramco faces a growing, structural threat that rarely makes the front page: the accelerating exodus of ESG investors.

As global capital increasingly prioritizes sustainability mandates, large institutional investors — pension funds, university endowments, sovereign wealth funds in Europe and North America — are systematically divesting from fossil fuels. This trend severely limits institutional ownership of Aramco stock, isolating the company from vast pools of patient, long-term capital.

The consequences are more significant than they appear. While Aramco generates staggering profits, its valuation and access to certain capital markets are constrained by its core business model. The company is increasingly reliant on domestic and regional investors, or sovereign wealth funds less bound by ESG mandates. This narrows the investor base and can create valuation discounts relative to what the underlying financials might otherwise justify.

There is a deeper strategic implication here. As ESG frameworks become more embedded in global financial regulation — particularly in Europe — the cost of capital for hydrocarbon businesses will structurally increase over time. Aramco's low production cost is a powerful buffer, but it does not make the company immune to the long-term repricing of climate risk in financial markets.

The Final Verdict: Lowest Cost, Largest Reserves, Longest Runway

Saudi Aramco's strategy is a masterclass in leveraging structural advantages while navigating existential threats. They are betting that the energy transition will be a marathon, not a sprint — and they have the stamina to win it.

Their core strategic bet is clear: grow petrochemicals, lock in Asian supply contracts, maintain OPEC+ discipline, and outlast higher-cost producers. Lowest cost. Largest reserves. Longest runway.

But the critical question that no one can answer with certainty is this:

Can Aramco generate enough cash to fund Saudi Arabia's post-oil future before the global economy fundamentally shifts away from hydrocarbons?

The race is on, and Aramco is running it on their own terms. The last barrel will undoubtedly be the most profitable. The only question is whether the finish line arrives before the world stops needing it.

Download the full Saudi Aramco SWOT Analysis PDF and explore the complete strategic framework behind this breakdown. It's free, clean, and built for strategists who think in systems.

Saudi Aramco SWOT Analysis PDF

If you found this valuable, subscribe to the StrategyPunk newsletter — concise, counter-intuitive strategy analysis on the world's most important companies, delivered straight to your inbox. No noise. Just signal.