Decoding Palantir: A Strategy House Analysis of the AI Operating System

Palantir has repositioned from defense contractor to AI OS provider. Here's how their strategy breaks down using the Strategy House framework.

Introduction

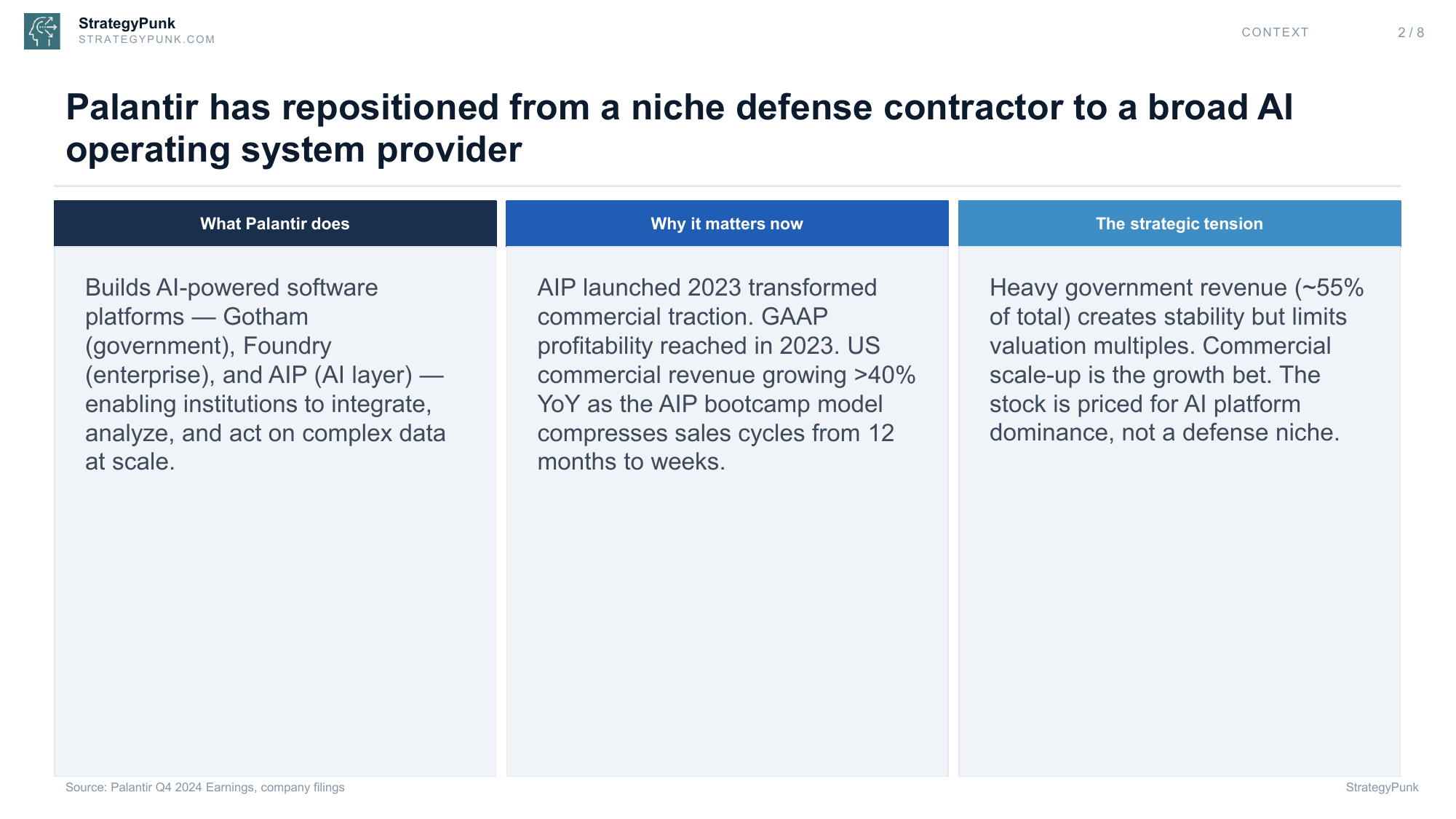

Palantir has fundamentally repositioned itself. For years, the market viewed the company through a narrow lens: a secretive, bespoke defense contractor building tools for the intelligence community. That narrative is dead. Today, Palantir is executing a ruthless, calculated pivot to become the default artificial intelligence operating system for the world's most critical institutions.

This shift is not just marketing. The launch of the Artificial Intelligence Platform (AIP) in 2023 marked an inflection point, driving commercial traction that finally pushed the company to GAAP profitability.

The US commercial business is soaring, up over 40% year-over-year. Why?

Because Palantir cracked the enterprise sales cycle. Their AIP bootcamp model compresses what used to be a grueling 12- to 18-month procurement slog into a matter of weeks.

Yet, a strategic tension remains. Government contracts still account for roughly 55% of total revenue. This base provides incredible stability and downside protection, but government revenue doesn't command the astronomical valuation multiples tech investors crave. To justify its current market cap, Palantir must scale its commercial operations aggressively. The stock is priced for absolute AI platform dominance, not a comfortable defense niche.

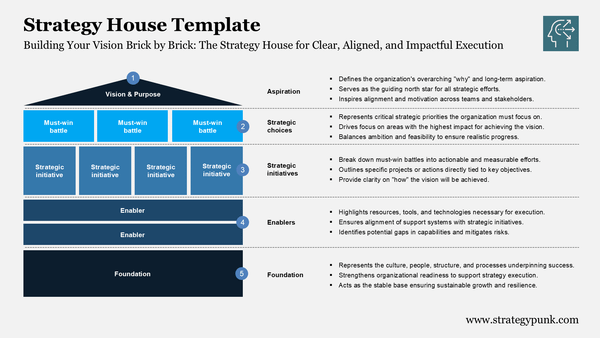

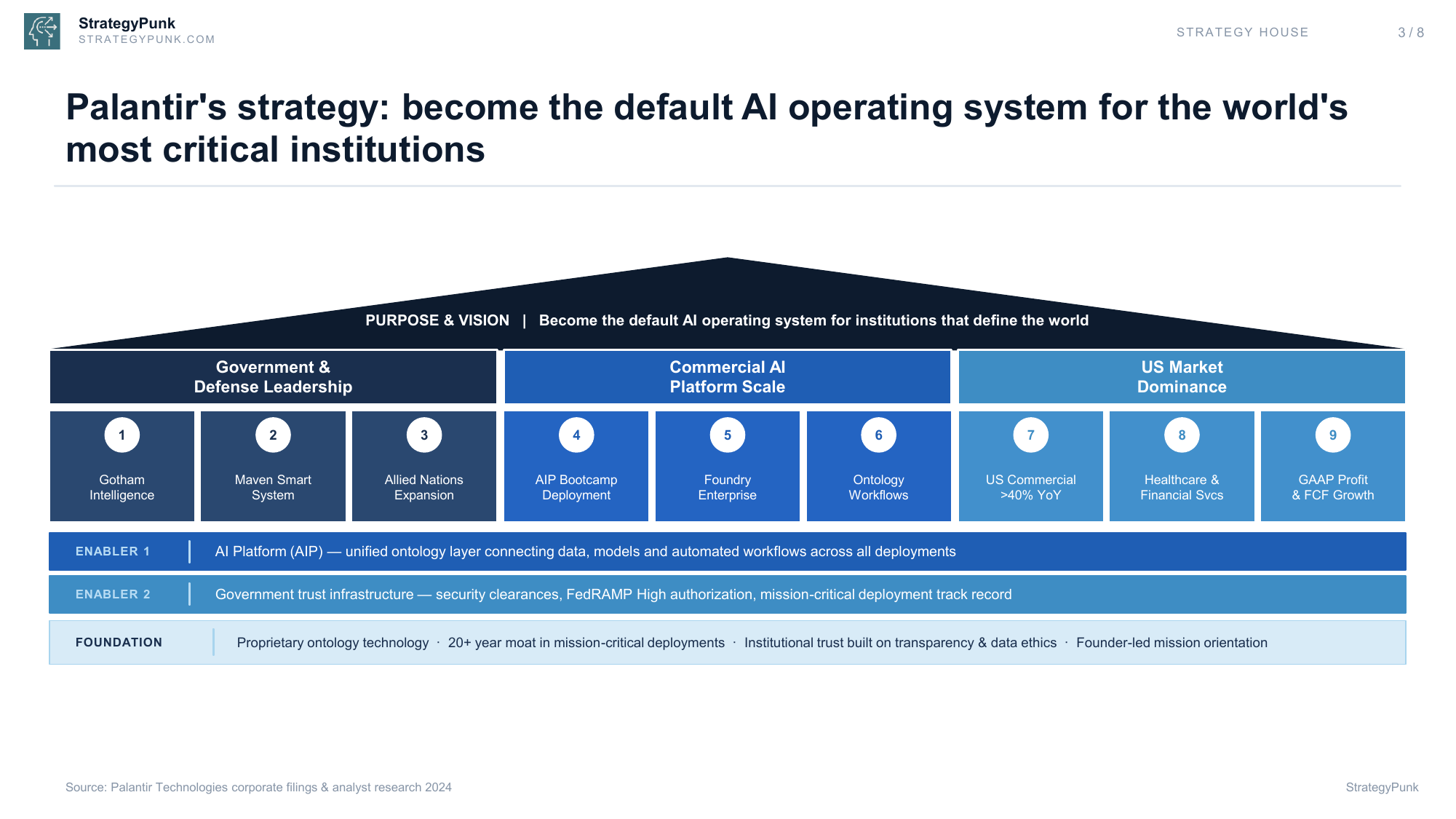

To understand how Palantir plans to bridge the gap between its defense origins and its commercial ambitions, we break down its approach using the Strategy House framework. This model breaks down their vision into concrete pillars, supported by unique enablers and a strong foundation.

This analysis uses the Strategy House framework — a one-page strategic structure that organizes a company's vision, must-win battles, strategic initiatives, enablers, and foundation into a single, visual architecture. It is widely used by McKinsey, Bain, and BCG to align leadership teams and stress-test strategic choices. Read the full framework guide and download the free template →

The Strategy House: Building the Default AI OS

Palantir's core purpose is ambitious: to become the default AI operating system for institutions that define the world. They aren't building lightweight SaaS apps for SMBs. They are targeting the apex predators of the global economy and the geopolitical landscape.

This vision rests on three distinct pillars:

- Government & Defense Leadership: Defending the core and expanding into allied nations.

- Commercial AI Platform Scale: Using AIP to penetrate the enterprise market at unprecedented speed.

- US Market Dominance: Winning the most lucrative software market on earth through deep sector expertise.

These pillars are supported by two key enablers: the AIP unified ontology layer and a strong government trust infrastructure. Everything is built on a foundation of proprietary technology, a 20-year moat in mission-critical deployments, and a founder-led mission orientation. Let's examine each component.

Pillar 1: Government & Defense Leadership

Palantir's government and defense segment is the bedrock of the company. Built over two decades, this is the highest-margin, most defensible revenue base in the enterprise software sector. It generated $1.85 billion in FY2024, representing 55% of total revenue.

The defense strategy hinges on three specific initiatives.

First is Gotham, the intelligence and defense analytics platform. Gotham has been the core operating system for the US intelligence community and the Department of Defense since 2003. It excels at integrating massive volumes of structured and unstructured data for mission planning and targeting. The lock-in here is profound. Government agencies do not rip and replace mission-critical targeting software. These are multi-year contracts with near-perfect renewal rates, driving a US government revenue base of $1.11 billion in FY2024, growing at a steady 12% year-over-year.

Second is the Maven Smart System. Palantir secured a $178 million contract in 2023 to serve as the AI operating layer for US military modernization. Maven focuses on real-time sensor fusion, algorithmic targeting recommendations, and logistics optimization. This moves Palantir from a back-office analytics tool to a front-line operational necessity. As the military digitizes the battlefield, Palantir is positioning itself as the central nervous system of that transformation.

Third is Allied Nations Expansion. The US cannot fight alone, and its software architecture must extend to its allies. Palantir is expanding Gotham deployments across the UK, NATO partners, and notably, Ukraine. The conflict in Ukraine has served as a grim but highly effective real-world proving ground for Palantir's battlefield AI capabilities. When allied nations see the platform perform in high-intensity conflict, the procurement conversation changes. This international government segment generated $737 million in FY2024, growing at 13%.

The financial profile of this pillar is exceptional. With an adjusted operating margin of around 34% and average agency relationships exceeding 20 years, the government funds the commercial expansion. It is a fortress that competitors like Microsoft or Salesforce cannot easily breach, protected by layers of security clearances and bespoke integration requirements.

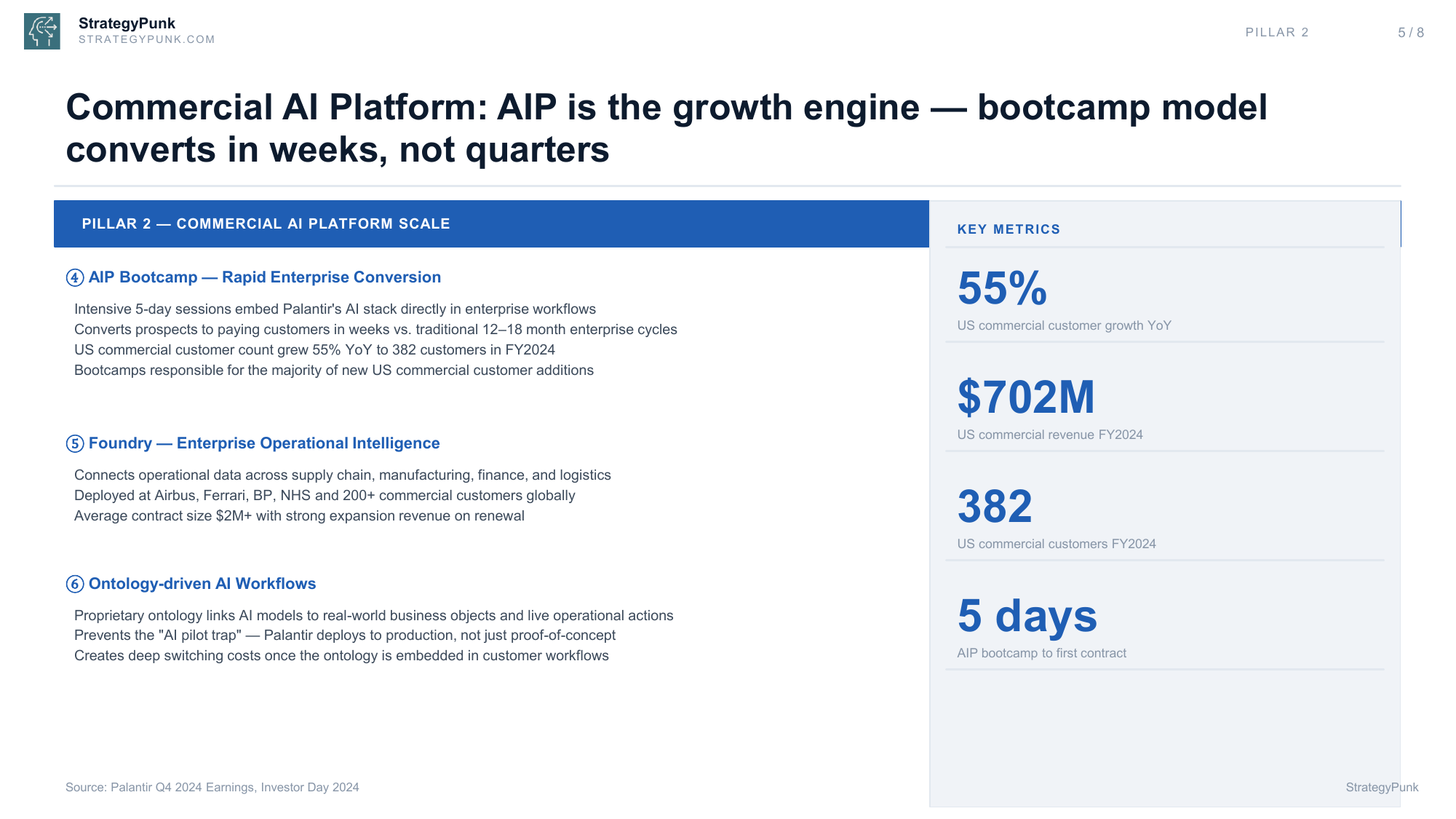

Pillar 2: Commercial AI Platform Scale

If the government business is the fortress, the commercial AI platform is the growth engine. This is where Palantir must win to justify its valuation. The strategy here is entirely built around velocity and time-to-value.

The defining innovation of this pillar is the AIP Bootcamp. Historically, Palantir's biggest weakness was its sales motion. Deploying Foundry required forward-deployed engineers, massive upfront costs, and a sales cycle that stretched over a year. The AIP bootcamp obliterates that friction. These intensive, five-day sessions embed Palantir's AI stack directly into a prospective customer's live workflows.

Engineers sit with the client, connect real data, and build a functioning AI use case in under a week. The conversion rate is staggering. This model transitions prospects to paying customers in weeks. In FY2024, US commercial customer count surged 55% year-over-year to 382 customers, with bootcamps driving the vast majority of those additions. The go-to-market motion has finally caught up with the technology.

The second initiative is Foundry, the enterprise operational intelligence platform. Foundry connects siloed operational data across supply chains, manufacturing floors, finance departments, and logistics networks. It is deployed at a massive scale within industrial giants such as Airbus, Ferrari, and BP. These are not small deals; average contract sizes easily exceed $2 million, and the expansion revenue upon renewal is incredibly strong as customers find new use cases for the integrated data.

The third initiative, and perhaps the most misunderstood by the broader market, is Ontology-driven AI Workflows. Most enterprise AI initiatives fail. They get stuck in the "pilot trap"—cool demos that hallucinate when exposed to real business logic and fail to integrate with legacy systems. Palantir's proprietary ontology solves this. The ontology links AI models to real-world business objects (a factory machine, a supply chain route, a specific employee) and connects them to live operational actions.

Palantir deploys AI to production. They build systems that take action, rather than just generating text summaries. Once a company embeds this ontology into its daily operations, the switching costs become insurmountable. Ripping out Palantir means ripping out the enterprise's digital nervous system.

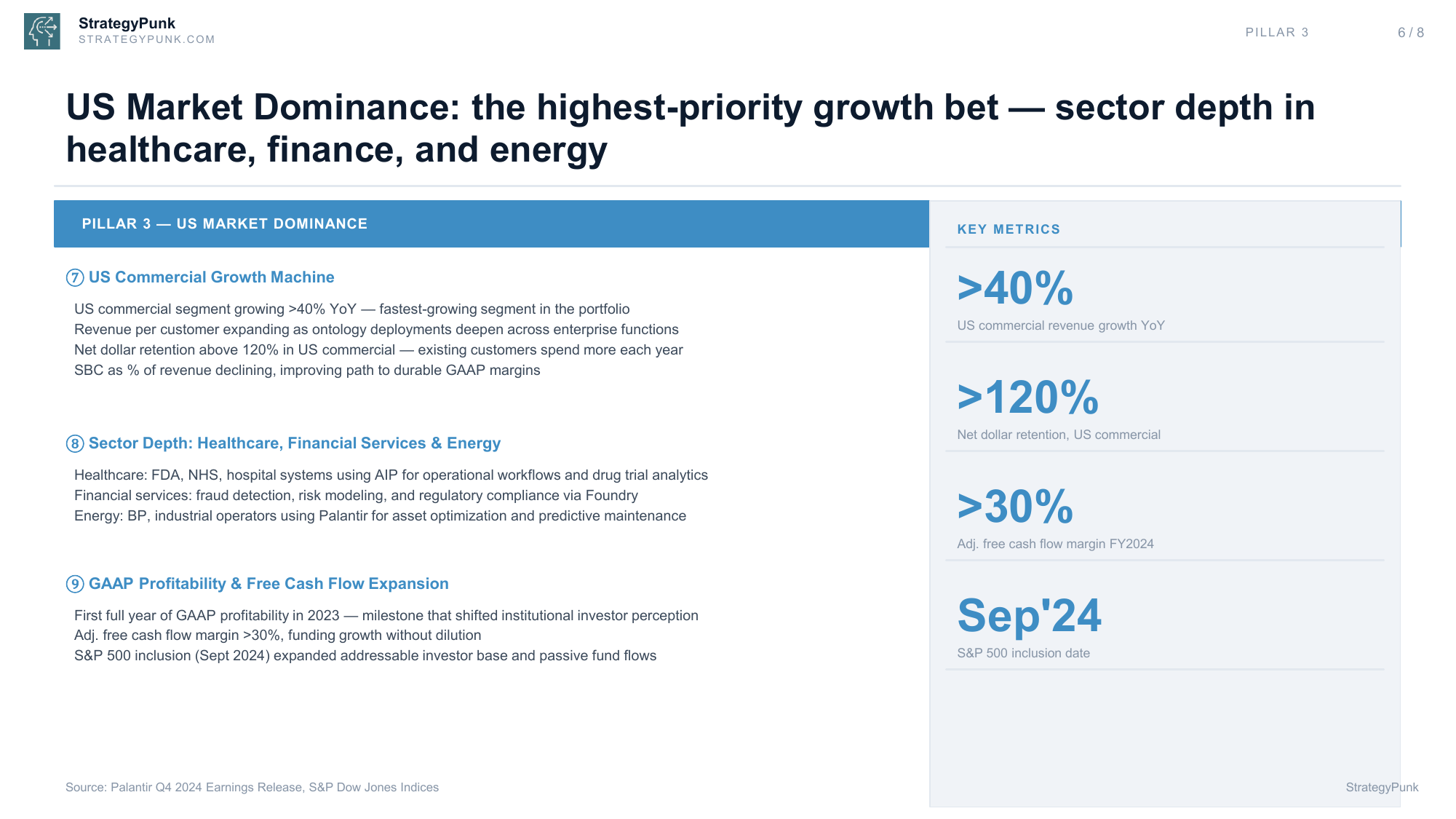

Pillar 3: US Market Dominance

Palantir has correctly identified the US commercial market as its highest-priority growth bet. The European market is fragmented, highly regulated, and slower to adopt aggressive AI operational models. The US is where the scale and the capital reside.

The US Commercial Growth Machine is currently the fastest-growing segment in the portfolio, expanding at over 40% year-over-year and generating $702 million in FY2024. The unit economics are improving rapidly. Revenue per customer expands as ontology deployments deepen across various enterprise functions. The net dollar retention rate sits comfortably above 120%, indicating that once a customer signs up, they consistently spend more each year. Stock-based compensation as a percentage of revenue is declining, which supports durable GAAP margins.

To achieve this dominance, Palantir is pursuing a Sector Depth strategy, focusing intensely on healthcare, financial services, and energy.

In healthcare, the complexity of data integration is massive. Palantir is deployed at the FDA, the NHS, and major US hospital systems, where it uses AIP to optimize operational workflows, manage bed capacity, and accelerate drug trial analytics.

In financial services, Foundry is used for high-stakes, compute-intensive tasks such as fraud detection, risk modeling, and regulatory compliance. Banks cannot afford AI hallucinations; they require the deterministic, auditable workflows that Palantir provides.

In the energy sector, industrial operators like BP use Palantir for asset optimization and predictive maintenance. When a single day of downtime on an oil rig costs millions, the ROI on an effective operational AI platform is immediate.

The final initiative in this pillar is GAAP Profitability & Free Cash Flow Expansion. Achieving its first full year of GAAP profitability in 2023 was a watershed moment. It fundamentally shifted institutional investor perception, moving Palantir from a speculative growth story to a maturing software giant. With an adjusted free cash flow margin exceeding 30%, the company is now funding its own hyper-growth without diluting shareholders. The inclusion in the S&P 500 in September 2024 further validated this transition, expanding the addressable investor base and triggering massive passive fund flows into the stock.

Enablers & Foundation: The Irreplaceable Moat

A strategy is only as strong as the assets that enable it. Palantir possesses two structural advantages that competitors cannot simply buy or build quickly.

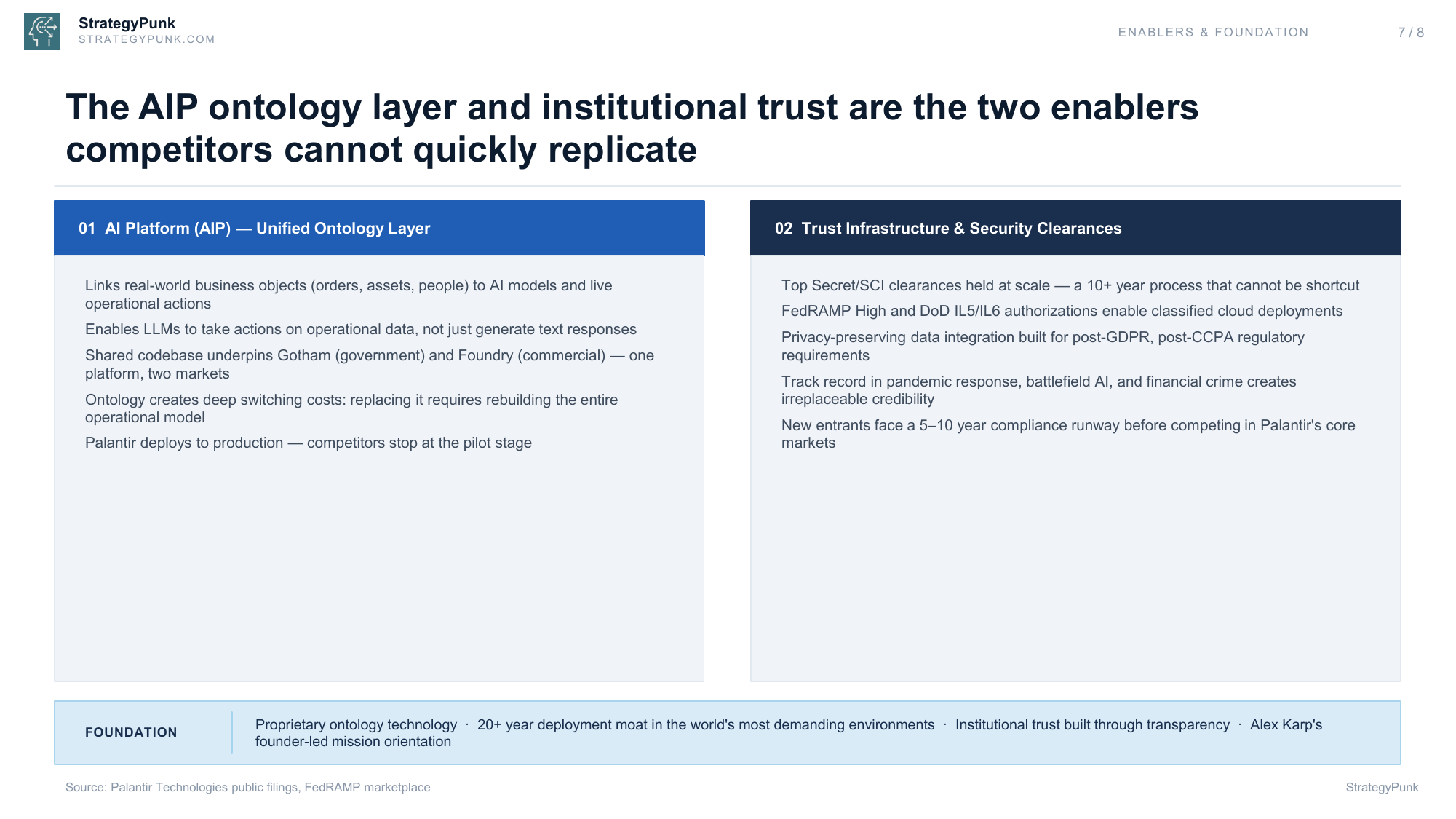

Enabler 1: The AI Platform (AIP) Unified Ontology Layer

The ontology is the secret to Palantir's success. Large Language Models (LLMs) are commoditizing. The value is no longer in the model itself, but in the connective tissue between the model and the enterprise. The ontology links real-world business objects to AI models and live operational actions. It enables LLMs to execute tasks using operational data, rather than just acting as glorified chatbots.

Crucially, Palantir uses a shared codebase underpinning both Gotham and Foundry. It is one core platform serving two distinct markets, driving massive R&D efficiency. As mentioned earlier, this ontology creates deep switching costs. Replacing Palantir requires rebuilding the entire operational model of the business. While competitors are selling AI pilots, Palantir is selling production-grade operational transformations.

Enabler 2: Trust Infrastructure & Security Clearances

You cannot fake trust in the defense sector. Palantir holds Top Secret/SCI clearances at scale. Building this workforce and securing these facilities is a decade-long process that new entrants cannot shortcut. Their FedRAMP High and DoD IL5/IL6 authorizations enable them to deploy in classified cloud environments that are off-limits to standard SaaS providers.

Their data integration architecture was built from day one to handle the most sensitive intelligence data on earth. This translates perfectly to the commercial sector, where privacy-preserving architecture is required to navigate post-GDPR and post-CCPA regulatory environments. Their track record in pandemic response, battlefield AI, and financial crime creates irreplaceable credibility. A startup pitching a defense AI tool faces a five- to ten-year compliance runway before it can even bid against Palantir.

The Foundation

Our foundation is proprietary technology and a 20-year deployment moat built in the world's most demanding environments. This institutional trust is anchored by transparency and data ethics. Finally, the company remains focused on Alex Karp's founder-led mission. Palantir operates with a philosophical intensity rarely seen in Silicon Valley, explicitly aligning itself with Western democratic values and refusing to do business with adversarial nations. This ideological stance is a feature, not a bug, deeply cementing its relationship with the US government and its allies.

Strategic Outlook: Justifying the Premium

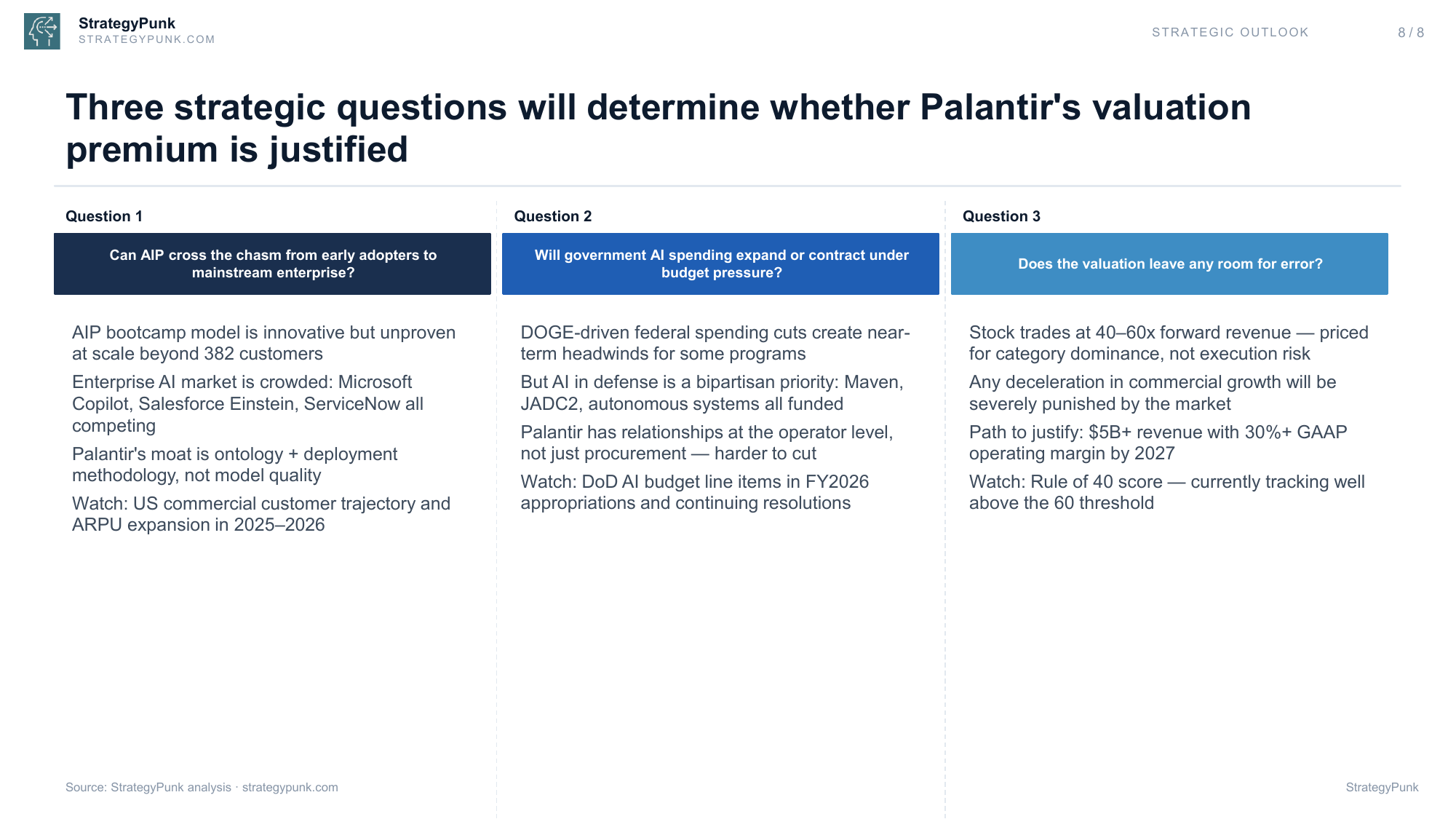

Palantir's strategy is clear, aggressive, and currently working. However, the market has priced the stock for perfection. Trading at 40 to 60 times forward revenue, the valuation assumes category dominance and leaves zero room for execution risk. Three critical strategic questions will determine whether this premium is justified over the next 36 months.

Question 1: Can AIP cross the chasm from early adopters to mainstream enterprise?

The bootcamp model is incredibly innovative, but it remains unproven at a massive scale. Growing from 382 US commercial customers to 3,000 requires a different level of operational leverage. The enterprise AI market is becoming fiercely crowded. Microsoft Copilot, Salesforce Einstein, and ServiceNow are all pushing their own AI narratives. Palantir must continually prove that its moat lies in its ontology and deployment methodology, not just access to models. We must closely monitor the US commercial customer trajectory and ARPU (Average Revenue Per User) expansion through 2025 and 2026.

Question 2: Will government AI spending expand or contract under budget pressure?

With potential DOGE-driven federal spending cuts looming, there are near-term headwinds for broad government software procurement. However, AI in defense remains a rare bipartisan priority. Programs like Maven, JADC2 (Joint All-Domain Command and Control), and autonomous systems are fully funded. Palantir has cultivated deep relationships at the operator level—with the soldiers and analysts who actually use the software—not just with procurement officers. Software loved by the operators is much harder to cut. The key metric to watch will be DoD AI budget line items in the FY2026 appropriations.

Question 3: Does the valuation leave any room for error?

Simply put, no. The market will severely punish any deceleration in commercial growth. To justify its current trajectory, Palantir needs to hit $5 billion in revenue with a 30% GAAP operating margin by 2027. They are currently tracking well above the Rule of 40 threshold, but maintaining that velocity as the revenue base expands is the ultimate test of their go-to-market strategy.

Palantir has successfully navigated the transition from a shadowy defense contractor to a highly profitable AI platform company. The Strategy House reveals a business built on deep technological moats and a rapidly accelerating commercial engine. The product works. The sales motion is fixed. Now, it is entirely a question of execution at scale.