SpaceX SWOT Analysis: Launch Monopoly, Internet Machine, and The IPO of the Century

SpaceX is more than a rocket company. Unpack the launch monopoly, Starlink cash engine, and massive IPO ambition. Free PDF download.

Introduction

If you're tracking aerospace, connectivity, or the next major public-market event, your focus needs to be on Hawthorne, California. SpaceX is no longer just a rocket company. It's three distinct behemoths rolled into one: a launch monopoly, a global satellite internet machine, and an emerging AI infrastructure bet.

We recently conducted a comprehensive SWOT analysis of SpaceX for StrategyPunk.com. The findings reveal a company moving at breakneck speed toward an unprecedented $1.75 trillion IPO, fueled by Starlink's cash flow and the sheer dominance of the Falcon 9. But the road ahead isn't without significant turbulence.

Here is the strategic breakdown of where SpaceX stands today, the massive opportunities it's chasing, and the critical risks that could disrupt its trajectory.

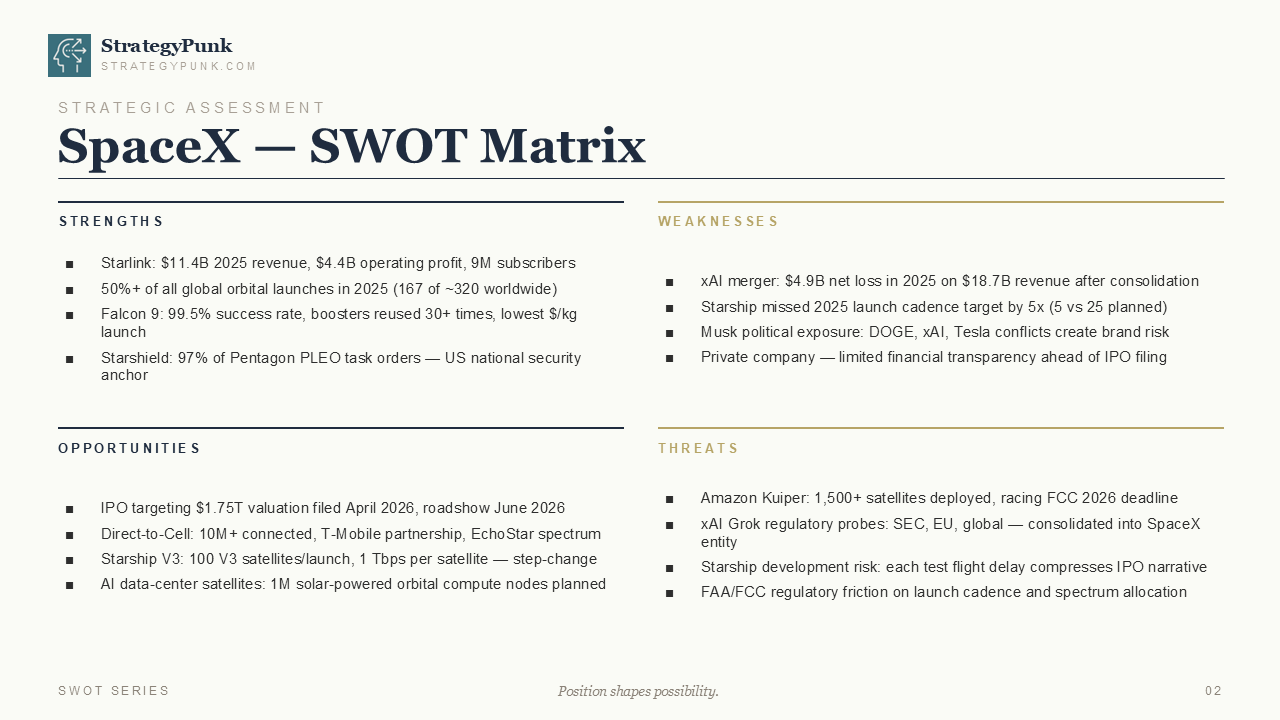

Strengths: The Foundation of Dominance

SpaceX's current market position is practically unassailable in the near term. The company has systematically dismantled the traditional launch market and built a recurring revenue engine.

The Launch Monopoly

Look at the numbers. SpaceX is projected to execute over 50% of all global orbital launches in 2025. That is 167 out of approximately 320 launches worldwide. This isn't just market leadership; it's a structural monopoly. The workhorse behind this is the Falcon 9. With a 99.5% success rate and boosters being reused 30+ times, SpaceX has achieved the lowest cost per kilogram to orbit in history. They have commoditized access to space, and everyone else is paying their toll.

The Starlink Cash Machine

Rockets are expensive, but Starlink is the economic engine making the Mars ambition viable. For 2025, Starlink is projecting $11.4 billion in revenue and $4.4 billion in operating profit, driven by an expanding subscriber base of 9 million. This is a high-margin, recurring-revenue business built on a launch monopoly.

The Ultimate National Security Anchor

SpaceX isn't just a commercial entity; it's deeply integrated into US national security. Starshield, the military-focused iteration of Starlink, has secured 97% of the Pentagon's Proliferated Low Earth Orbit (PLEO) task orders. When the Department of Defense relies on your infrastructure to this degree, you possess an immense strategic moat.

Weaknesses: The Cracks in the Armor

Despite the overwhelming strengths, the foundation has stress points. The integration of Elon Musk's broader empire and the sheer ambition of the engineering targets create substantial internal risks.

The xAI Consolidation Drag

The recent merger with xAI brings significant financial baggage. Post-consolidation, the entity is looking at a $4.9 billion net loss in 2025 on $18.7 billion in revenue. While the AI play is strategically interesting, it severely impacts the near-term profitability narrative heading into an IPO.

Starship Development Delays

Starship is the linchpin of SpaceX's future, but it is missing targets. The company missed its 2025 launch cadence target by a factor of five, achieving only 5 launches against a planned 25. Hardware development is hard, but when your valuation depends on rapid iteration, missing cadence targets is a glaring weakness.

The Key Man Risk and Brand Exposure

Elon Musk is SpaceX's greatest asset and its most unpredictable liability. His political exposure, the Department of Government Efficiency (DOGE) involvement, and the intertwined nature of xAI and Tesla create undeniable brand risk. For institutional investors considering a public offering, this volatility warrants a steep risk premium.

Financial Opacity

As a private company, financial transparency is limited. While leaks and projections paint a rosy picture of Starlink, the actual consolidated financials remain opaque ahead of the official IPO filing. Public markets demand predictability, and SpaceX currently operates in the shadows.

Opportunities: The Path to $1.75 Trillion

If SpaceX executes on its roadmap, the upside is historic. The company is positioning itself not just to dominate space, but to reshape global telecommunications and AI infrastructure.

The IPO of the Century

The numbers being floated are staggering. SpaceX is targeting a $1.75 trillion valuation, with an S-1 filing anticipated in April 2026 and a roadshow in June 2026. If successful, this will be a watershed moment for public markets, offering investors a chance to buy into the infrastructure of the future.

Direct-to-Cell Expansion

Starlink is moving beyond dish antennas. The Direct-to-Cell initiative, backed by a partnership with T-Mobile and utilizing EchoStar spectrum, aims to connect over 10 million devices directly. This effectively turns SpaceX into a global mobile carrier, bypassing traditional ground infrastructure entirely.

Starship V3 and the Cost Revolution

Starship V3 is the holy grail. The goal is to deploy 100 V3 satellites per launch, with each satellite offering 1 Tbps of capacity. This represents a step-change in capability. If Starship achieves reliable cadence, it will drop the cost-to-orbit to sub-$100/kg. This is the metric that makes the $1.75 trillion valuation defensible.

Orbital AI Compute

The xAI merger starts to make sense when you look at the long-term vision: AI data-center satellites. SpaceX plans to deploy 1 million solar-powered orbital compute nodes. This would move massive data processing off-world, leveraging unlimited solar energy and the natural cooling of space.

Threats: The External Pressures

SpaceX is playing a high-stakes game, and external forces are aligning to challenge its dominance. Regulatory friction and deep-pocketed competitors pose serious threats.

The Kuiper Deadline

Amazon's Project Kuiper is the most credible threat to Starlink's dominance. Amazon is racing against an FCC deadline to deploy over 1,500 satellites by July 2026. With Jeff Bezos's backing, Kuiper has the capital to endure massive losses in pursuit of market share and to challenge SpaceX's pricing power.

Regulatory Probes and Friction

The xAI Grok integration brings regulatory heat. Probes from the SEC, the EU, and global regulators are scrutinizing the consolidated entity. Beyond AI, SpaceX faces ongoing regulatory friction from the FAA and FCC over launch cadence and spectrum allocation. Bureaucracy can slow down the rapid iteration cycle that SpaceX relies on.

The Starship Narrative Risk

Every test flight delay for Starship compresses the IPO narrative. The $1.75 trillion valuation relies on Starship working flawlessly and frequently. If development stalls, the market will re-evaluate the entire business model.

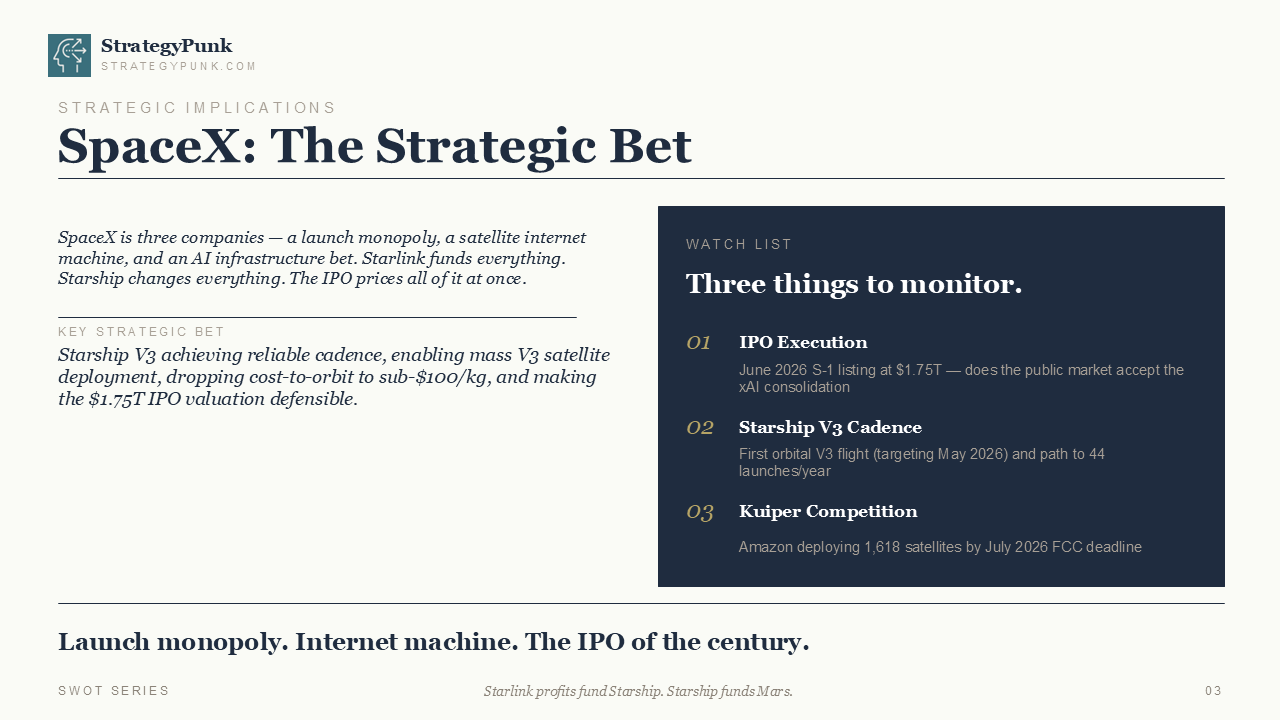

The Strategic Bet

SpaceX is placing a massive, multifaceted wager. The core strategic bet is this: Starship V3 must achieve a reliable launch cadence. This enables the mass deployment of V3 satellites, which drops the cost-to-orbit to sub-$100/kg, thereby making the astronomical $1.75 trillion IPO valuation defensible.

Starlink profits fund Starship. Starship funds Mars. It is an elegant, high-risk loop.

As we approach the anticipated June 2026 listing, the market must decide iwhether to acceptthe xAI consolidation and the inherent volatility of the Musk empire. The execution of the IPO, the cadence of Starship V3 (with the first orbital V3 flight targeted for May 2026), and Amazon's ability to meet its Kuiper deployment deadlines are the three critical factors to monitor.

SpaceX has redefined what is possible in aerospace. Now, it has to prove it can deliver the financial returns to match its engineering triumphs.

Want to dive deeper into the SWOT Analysis?

Download the full StrategyPunk SpaceX SWOT Analysis PDF below to get the complete breakdown of the metrics, the competitive landscape, and the strategic implications for the aerospace sector.

Download the SpaceX SWOT Analysis PDF

Stay ahead of the curve.

Join thousands of strategy professionals and get the latest deep dives, frameworks, and analyses delivered straight to your inbox.