ASML SWOT Analysis: The Quietest Moat in AI & 5 Counter-Intuitive Strategic Takeaways

ASML is the sole global supplier of EUV lithography — the machines that manufacture every leading-edge AI chip at TSMC, Samsung, and Intel. This SWOT analysis unpacks why its monopoly is protected by physics rather than capital. Download the free SWOT matrix PDF.

AI in a small Dutch town?

When we talk about the AI boom, the conversation almost always revolves around Nvidia’s GPUs, OpenAI’s models, or the hyperscalers building massive data centers. But beneath the surface of trillion-dollar valuations and generative AI breakthroughs lies a singular, physical bottleneck: ASML. Headquartered in Veldhoven, Netherlands, ASML holds a true natural monopoly on the extreme ultraviolet (EUV) lithography machines required to manufacture every leading-edge AI chip on the planet.

We recently conducted a deep dive into ASML’s strategic position, culminating in a comprehensive SWOT analysis. You can download the full, high-resolution ASML SWOT Matrix PDF at the bottom of this post.

But for now, let’s unpack the core SWOT elements and the most surprising, impactful, and counter-intuitive takeaways from our analysis. These aren't just industry talking points; they are the structural realities defining the future of technology.

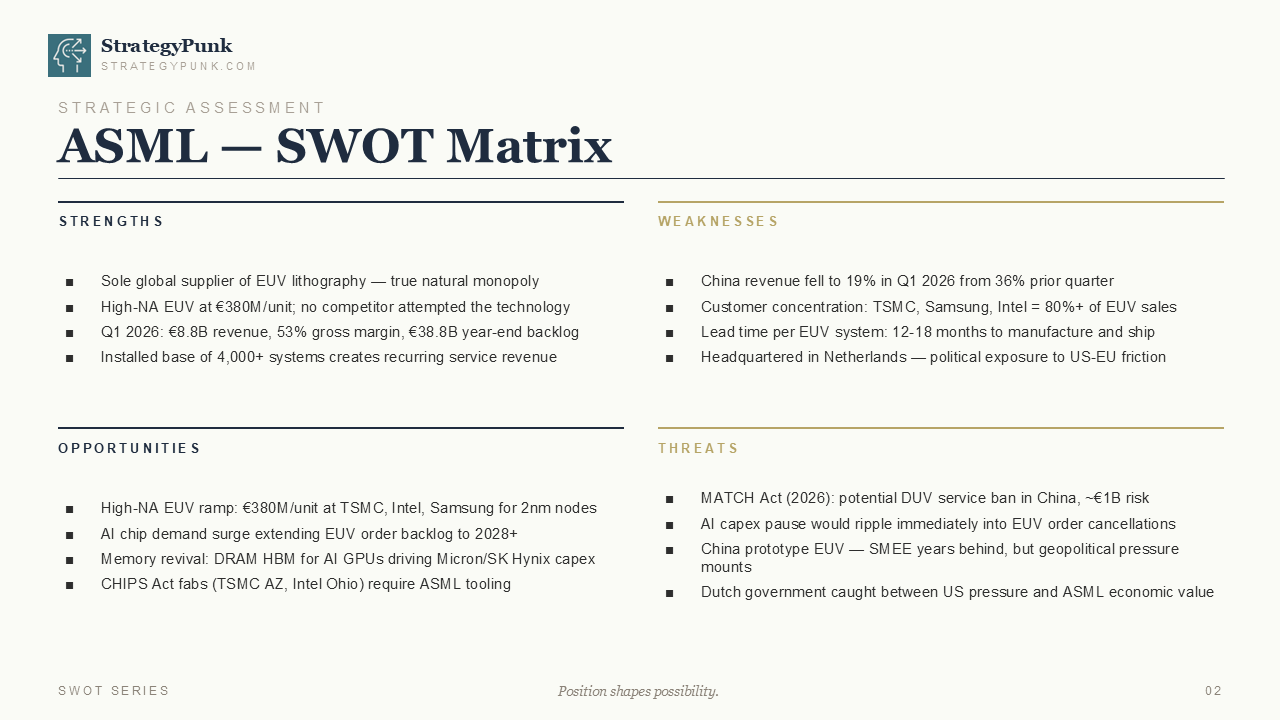

ASML SWOT Matrix Summary

1. The "China Risk" is Real, But The Margin Math is Better

ASML’s exposure to geopolitical tensions is often cited as its biggest vulnerability. The numbers back this up: China's revenue fell to 19% in Q1 2026, down from 36% the prior quarter [1]. The proposed MATCH Act threatens a deep-ultraviolet (DUV) service ban in China, putting roughly €1 billion at risk [1].

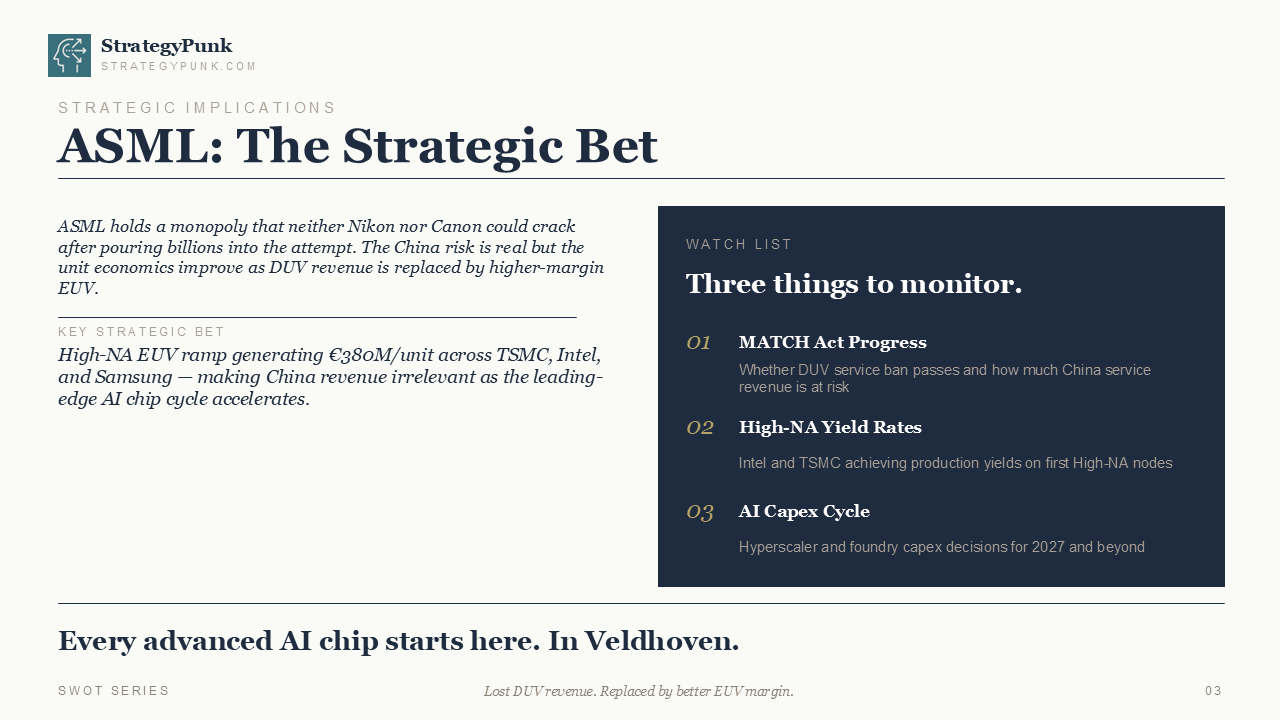

However, the panic over lost Chinese revenue misses the bigger strategic picture. The unit economics of ASML’s product line are shifting favorably. The revenue lost from older, lower-margin DUV systems that are restricted from entering China is being rapidly offset by the explosive growth of next-generation High-NA EUV systems.

These High-NA machines command an astonishing €380 million per unit [1]. As TSMC, Intel, and Samsung ramp up their 2-nanometer nodes, the sheer margin expansion from these mega-machines effectively neutralizes the top-line hit from China. The geopolitical risk is a headline grabber, but the underlying margin math is quietly making ASML a more profitable enterprise.

2. A Monopoly Protected by Physics, Not Just Capital

In the tech industry, we are used to seeing moats breached by well-funded competitors. NVIDIA faces challenges from AMD and custom silicon developed by Google and Amazon [2]. But ASML’s moat is entirely different.

Neither Nikon nor Canon could crack the EUV market, despite pouring billions into the attempt [1]. ASML’s CEO Christophe Fouquet recently stated that "no one is coming for us" [2]. This isn't corporate arrogance; it’s a statement of physical reality.

"A company could commit $20 billion to building an ASML competitor and still not have a functioning EUV machine at the end of the program, because the knowledge required to make the machine work is distributed across ASML’s 44,000 employees, its supply chain relationships, and 30 years of operational learning." [2]

Patents or capital requirements don't just protect ASML’s monopoly; it is protected by the sheer, accumulated difficulty of manipulating physics at an atomic scale. It is the narrowest bottleneck in the physical infrastructure of the AI economy.

3. The 18-Month Lag That Dictates the AI Capex Cycle

When hyperscalers decide to build a new AI data center, they trigger a supply chain reaction that ultimately ends in Veldhoven. But that reaction is slow.

The lead time for manufacturing and shipping a single EUV system is 12 to 18 months [1]. With an installed base of over 4,000 systems generating recurring service revenue, and a Q1 2026 year-end backlog of €38.8 billion [1], ASML’s production schedule is effectively locked in years in advance.

This means that any sudden surge—or pause—in AI capital expenditure has delayed, complex ripple effects. If AI chip demand surges, it simply extends ASML’s order backlog out past 2028. Conversely, an AI capex pause would eventually lead to cancellations of EUV orders. The strategic takeaway here is that ASML’s order book is the ultimate leading indicator for the physical build-out of the AI revolution. If you want to know what the AI hardware landscape will look like in 2028, look at ASML’s backlog today.

4. Customer Concentration is a Feature, Not a Bug

Our standard business strategy is to treat customer concentration as a significant risk. ASML, TSMC, Samsung, and Intel account for over 80% of EUV sales [1]. In almost any other industry, having your revenue tied to just three clients would be a red flag for investors.

But in semiconductor manufacturing, this concentration is a feature of the ecosystem's maturity. Only these three foundries have the scale, capital, and technical capability to utilize High-NA EUV technology. This tight triad creates a co-dependent relationship. TSMC cannot advance to the next node without ASML, and ASML needs TSMC’s massive capital expenditure to fund its own R&D.

This dynamic shifts competitive advantage toward the foundries with the deepest pockets and the earliest purchase commitments. NVIDIA’s current dominance is partly a downstream expression of TSMC’s wafer allocation, which is itself dictated by ASML’s machine delivery schedule [2].

5. The Memory Revival is the Silent Growth Engine

While the narrative is dominated by AI logic chips (like Nvidia's GPUs), the memory sector is undergoing a massive revival that directly benefits ASML.

The surge in AI compute requires massive amounts of High Bandwidth Memory (HBM). This is driving a new capex cycle for memory giants like Micron and SK Hynix [1]. To produce the dense DRAM required for HBM, these manufacturers are increasingly reliant on advanced lithography.

This creates a secondary, highly lucrative growth engine for ASML. Even if logic-chip demand were to normalize, the memory sector's desperate need to keep pace with AI processing speeds would provide a massive, under-discussed tailwind for EUV orders.

The Ultimate Strategic Bet

ASML is the only company building the machines that can build the future. A near-monopoly defines its strategic position, a product roadmap that naturally expands margins, and a central role in the most important technological arms race of our generation.

The ultimate question for strategists and investors isn't whether ASML will face a viable competitor—they won't anytime soon. The question is whether the global AI capex cycle can sustain the astronomical costs required to push physics to its absolute limits.

Will the demand for AI compute outpace ASML's ability to manufacture these modern marvels, making lithography the permanent constraint on human technological progress?

Download the Full Analysis

Want to dive deeper into the strategic forces shaping ASML? Download our complete, high-resolution SWOT matrix below.

ASML SWOT Analysis PDF

References

[1] ASML SWOT Analysis Matrix, StrategyPunk.com, 2026.

[2] "ASML’s CEO Says No One Is Coming for Them, and He Is Correct in a Way That Makes ASML the Quietest Moat in the Entire AI Supply Chain", Startup Fortune, May 6, 2026. URL: https://startupfortune.com/asmls-ceo-says-no-one-is-coming-for-them-and-he-is-correct-in-a-way-that-makes-asml-the-quietest-moat-in-the-entire-ai-supply-chain/